Interview with Mark Brennan, CEO and President of Sierra Metals Inc. (TSX: SMT): Canadian Polymetallic Producer with Tremendous Opportunity for Transformative, Organic Growth in Three Districts in Mexico and Peru

|

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 10/12/2016

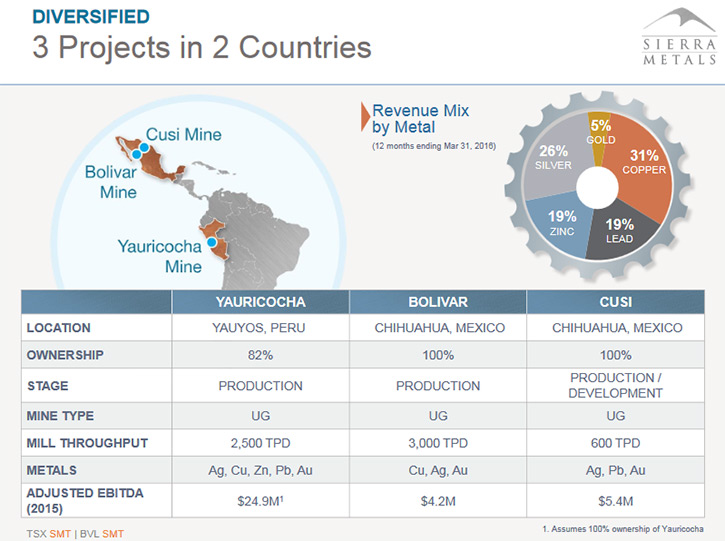

Sierra Metals Inc. (TSX: SMT) is a Canadian polymetallic producer with exciting resource growth potential. Mark Brennan, CEO and President of Sierra Metals Inc. (TSX: SMT), tells us they have a tremendous opportunity for transformative, organic growth. Sierra Metals Inc. has three districts: the Yauricocha in Peru, which includes a brand-new discovery and has 18,000 hectares, 15,000 hectares at Bolivar in Chihuahua State, Mexico, and 12,000 hectares at Cusi in Mexico. The Yauricocha discovery currently has 4,000,000 tons, measured & indicated. Mark believes Sierra could see multiples of this tonnage come out of this new discovery. Esperanza Zone appears to be accounting for 40% of their reserves and resources. Sierra is an old mine with revitalized growth, improved technology, comprehensive restructuring and renewed focus. Sierra Metals Inc. is a company to watch.

Dr. Allen Alper: This is Dr. Allen Alper, Editor-in-chief of Metals News, interviewing Mark Brennan, CEO and President of Sierra Metals Inc. Mark, could you tell our readers what differentiates Sierra Metals from other companies? I know you have great properties in Peru and also in Mexico. Tell me about your base metal and precious metal properties and how they're doing.

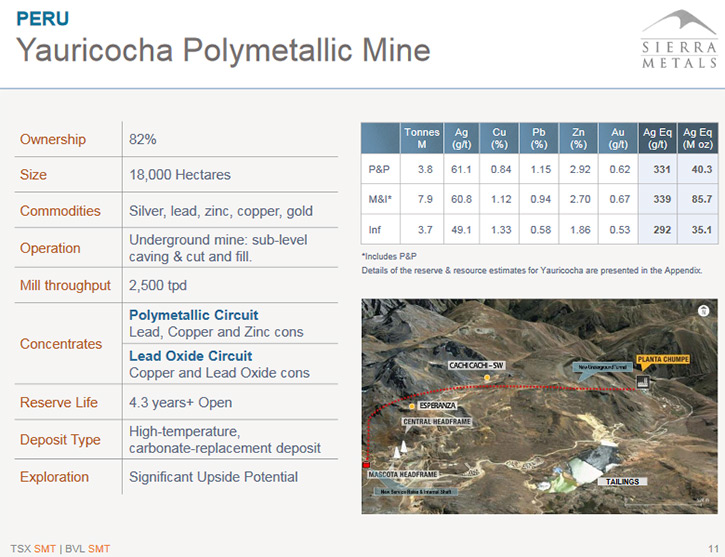

Mr. Mark Brennan: Thank you very much. I believe the differentiator between Sierra Metals and our peers is that Sierra Metals has tremendous, tremendous opportunity for transformative, organic growth. We have three districts: the Yauricocha in Peru, which is 18,000 hectares, 15,000 hectares at Bolivar in Chihuahua State, Mexico, and 12,000 hectares at Cusi in Mexico. In actual fact, we don't just have three mines; we have three districts.

At Yauricocha, we are only working currently on a fraction of the 18,000 hectares, a de minimis fraction of the whole entire property, and yet even this small area, which we're calling the central mining zone and the central mine area, has huge scope to increase dramatically the potential for resource growth at Yauricocha. In Yauricocha, we have a mine that's been producing for 70-odd years, now down to a depth of about, 600 to 700 feet below surface.

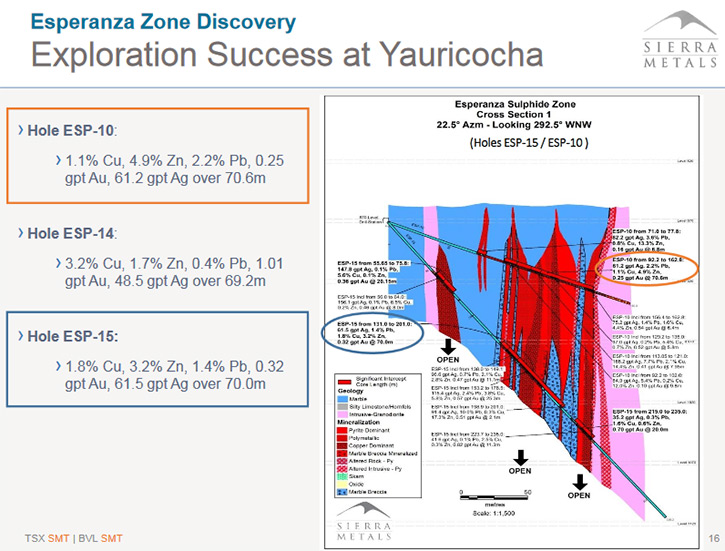

We recently found a brand new zone called Esperanza that we announced in January of 2016, a new discovery. We believe the Esperanza Zone is a drop fault from the central mine zone, which has been mined for the last 70 years. It's less than 100 meters from where we were mining, 400 meters from the actual Central Mine Zone itself.

We believe this Esperanza Zone is already accounting for 40% of our reserves and resources. We anticipate a significant increase from where we are today. We have 4,000,000 tons in the measured, indicated and third categories, and we believe that we could see multiples of this.

We've delineated the zone from the 870 level to the 970 level. That should be produced over the course of the next 18 months. We’ve also drilled below existing holes that we published. It's open to the north. It's open to the south, and it's open to depth. We see huge potential to increase our resources at Yauricocha significantly, from Esperanza alone.

We spent $600,000 discovering Esperanza. For 4,000,000 tons that's a huge benefit from the cost benefit analysis of capital. It is far cheaper to acquire through the drill bit than through acquisition.

We are doing brownfield exploration in a very nearby, porphyry system. We have a copper skarn system on top of Esperanza. We see just transformative growth through organic growth moving forward, which I don't think a lot of companies can say.

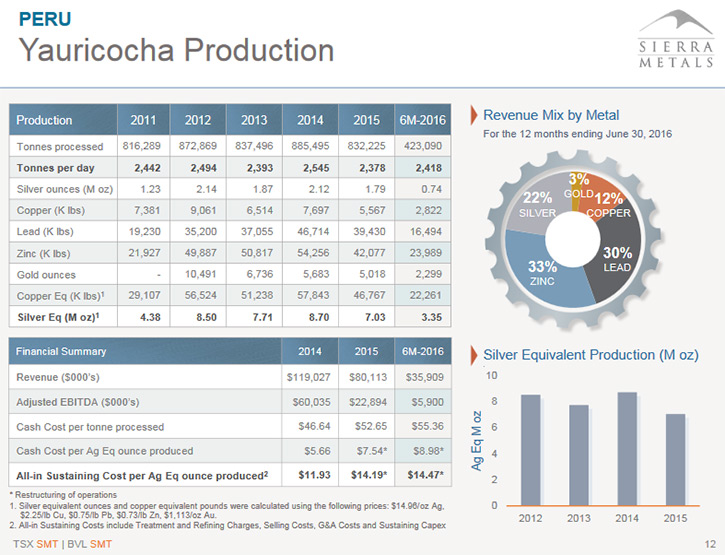

In the last 12 months at Yauricocha, we've come into the asset and restructured it. We started the restructuring in the third quarter of last year. We completed the restructuring in the second quarter of this year, as advertised. We announced in August that we had achieved record production for the 70-year history of the mine and we have also just announced a sequential record production month for Yauricocha for September.

Our focus is not only on production but also on value per ton of ore mined. Our first key driver is cash-flow and the value of the rock that we're producing. Obviously, as we produce more rock, it gives us better per-unit cost metrics. The second metric we're looking at is production growth. I'm very pleased to say, we've seen a 40% increase in our value-per-ton since the restructuring began. That's how we're going to continue focusing our attention to bring our costs back down to the previous levels.

We have a very well-oiled machine in the sense that the restructuring brought in new mining methodologies, new practices, and new technologies. For example, we've gone from steel set advancement to shotcrete, which means we're advancing three meters per shift as opposed to a meter per shift. We're seeing very, very strong development of the project itself from the foundation of the project. On top of that, we have this organic growth that I think is going to give transformational and multiples of net asset value growth.

Dr. Allen Alper: That's fantastic. That's really excellent progress. Could you tell me a bit more about what's happening in Mexico?

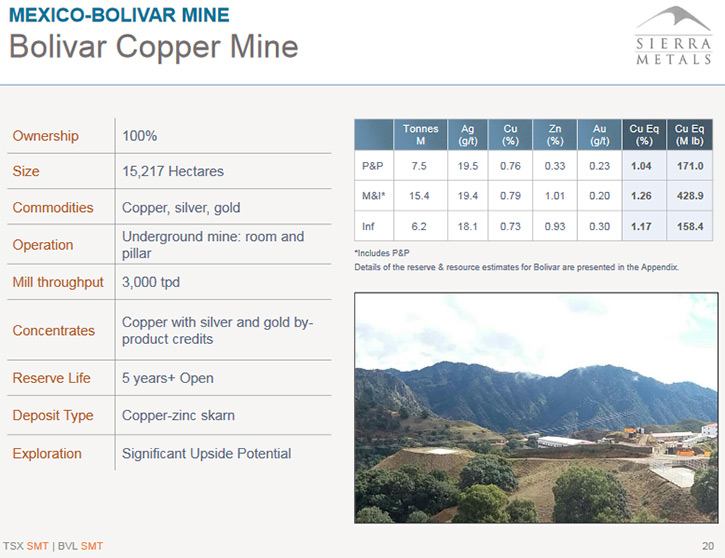

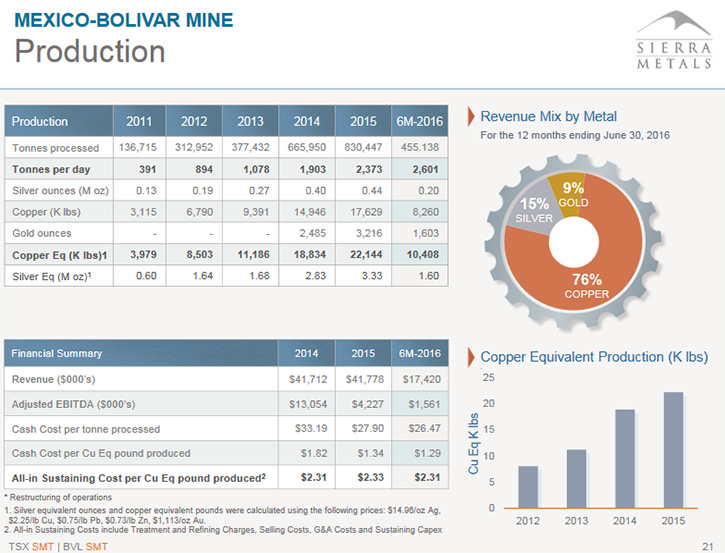

Mr. Mark Brennan: In Mexico, we've seen very good progress in terms of our increase in volume. That's been a very positive thing. At Bolivar the mine production is now approaching about 3,000 tons per day, wherein a year ago we were running closer to 2,100 to 2,200 tons per day.

We are seeing a reduction in grade. Very similar to Yauricocha, there has been very little emphasis on exploration and brownfield exploration to look at improving grade. That is now going to be the focus of our operations at Bolivar. We have three areas, immediately within the mining confines, that we believe we can bring to production within the next 6 to 12 months that can improve our grades dramatically.

We have an area called La Sidra, about four kilometers away, which looks very promising. We're working on proof of concept now, just like we did on Esperanza last year at Yauricocha. By the end of the year, we expect we'll have proof of concept at La Sidra, which looks to be a very interesting gold, zinc, lead area. We anticipate having multiples of grade, compared to where we're mining currently at Bolivar, which is running about 1 to 1.05% copper equivalent. We plan to bring La Sidra into the production schedule very quickly.

We also are targeting an area called Bolivar West, which is just on the other side of the fault from where we're mining currently, so almost directly adjacent to the mining operations we have now. That, again, looks like we're going back to our historical grade, which is a much higher grade, a multiple of where we are mining today. We're looking for proof of concept by year end. We’re also looking at Bolivar Noroeste, which is about 3 kilometers to the north, which we believe is one trend, a continuum of where we're mining today.

Our emphasis, moving forward on Bolivar, is less on volume growth and more on value per ton growth and grade improvement. That is our new focus on Bolivar. We're very excited. We think we can see the same type of transformational growth at Bolivar as we have successfully achieved in Yauricocha.

Dr. Allen Alper: That's excellent!

Mr. Mark Brennan: Yeah, very good.

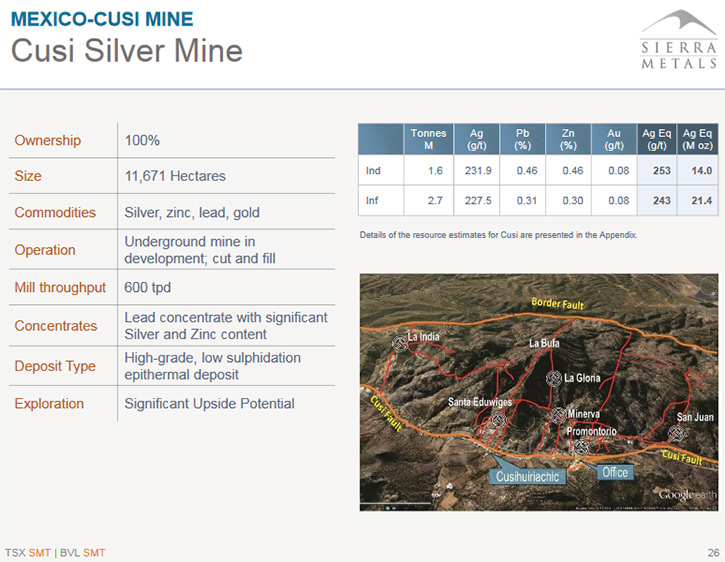

I'll talk very quickly about Cusi, which is the baby of the family. It's a quasi-development production story. We're producing around 600 tons per day currently. What's nice is the project has turned the corner. In the last three years, '13, '14 and '15, we expended about $15,000,000 on the project. This year the project now looks like it will be stand-alone, certainly breaking even, hopefully, making a little bit of money. We will not be spending the amount of capex going forward at Cusi.

We think this area, a district of 12,000 hectares, and this mine have substantial potential. We see a similar project called Los Gatos, owned by Sunshine Silver Mining and Refining, about 35 miles southwest of Cusi. They're deeper into the system then we are currently.

It looks like, as we go deeper, we're moving away from narrow vein mining. Currently, we're mining half a meter to one meter mine veins, which is very difficult. We're mining from probably about 25 different faces. What we plan to do is go deeper. We're starting to see evidence of ballooning of the veins and so seeing wider structures, 6 to 8 meters in width in areas. We're starting to see more polymetallics, some zinc and some lead.

We hope we're going to see wider widths, more consistent widths combined with equal silver but contributing zinc and lead, which is very similar to what we see down at Los Gatos. It is very exciting to us and something that we're looking to grow dramatically over the course of the next few years.

Dr. Allen Alper: That's excellent! Could you tell me a bit more about your overall cash-flow?

Mr. Mark Brennan: Sure. Last year we did about 33,000,000 of cash-flow. This year we've targeted the same kind of number. Now it's looking very positive that we should surpass those numbers. Very positive! We have $30,000,000 of cash in the bank approximately. The objective that Sierra Metals and I have as CEO, is to take the company back to cash-flow and EBITDA levels that we saw in 2014, when commodity prices were much higher, when we were generating around 75,000,000 in cash-flow.

I think, with the restructuring we've had at Yauricocha, and the improvements we're making at Bolivar and Cusi, that's a very realistic target for the next couple of years.

Dr. Allen Alper: Excellent! Could you tell me a bit about how your overall costs compare to some of your peers?

Mr. Mark Brennan: At Yauricocha, we've seen costs move higher as a consequence of the restructuring. We had to drill irrigation holes to solve some water issues. When we did the restructuring, our volumes dropped from about 2,500 tons a day, down to as little as 1,800 tons a day. But with our improved procedures, I expect our costs to go down to historical levels and lower. My target on costs, particularly at Yauricocha, is to see something with a 10 in front of it, and I think that's highly achievable with the higher value ore that we're seeing combined with the increased volumes.

Dr. Allen Alper: Very good. Could you tell us a little bit about your background, your team, your board?

Mr. Mark Brennan: We have a very experienced team throughout the whole organization. The board is led by a chairman, who's a third-generation engineer, with three mining engineering degrees and a history of family mining. One of our board members, formerly ran Teck Corporation, one of the largest mining companies in Canada. We have a very strong financial, technical board component.

At the management level, we have a very, very experienced operational team, very well-versed in restructuring, rolling up their sleeves and turning operations around. That includes both the operational side and the management side. We have a very strong group at the corporate level, with the executive suite, financing, all facets of management. We're very comfortable that we have a very strong and very deep team of very experienced technical and financial individuals to take the assets forward.

Dr. Allen Alper: That sounds great. Could you tell me a bit more about yourself, Mark? I know you have a great career. You've accomplished great successes.

Mr. Mark Brennan: I'm an economist and went into investment banking. In the early 2000's, I moved into the acquisition and development of new companies. My role since early 2000 has been coming into companies, helping restructuring them, turning them around, growing and building them. I built a company called Largo Resources from a hole in the ground to a producing asset. My experience is in management. I'm very financial.

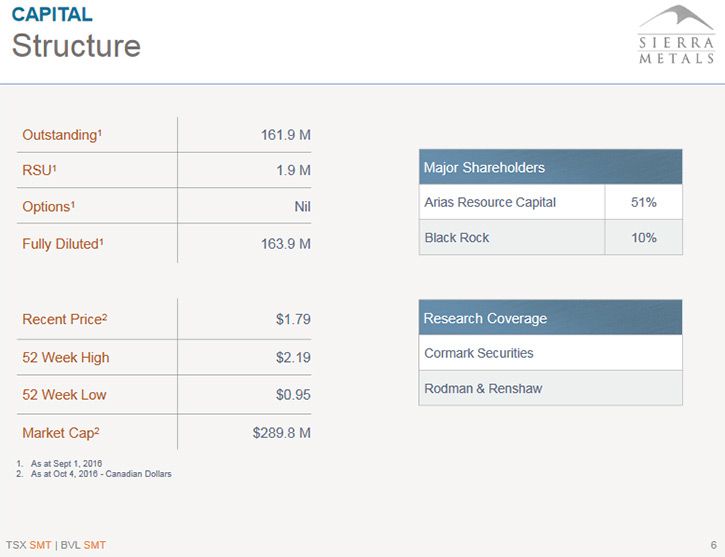

Dr. Allen Alper: That's excellent. Could you tell us a bit more about your Share Structure and your Capital Structure?

Mr. Mark Brennan: We have 162,000,000 shares, 164,000,000 shares, fully diluted. We have a Market Cap of approximately $325,000,000. We have very attractive debt of 85,000,000. We hope we'll bring that debt down by 20,000,000 over the course of the next year. We'd like it to be at that one-to-one ratio to EBITDA. We think that in 2017 we should accomplish that goal.

Dr. Allen Alper: That's very good. What are the primary reasons our high-net-worth readers/investors should consider investing in Sierra Metals?

Mr. Mark Brennan: I think the first and primary reason is that Sierra Metals is cheap. I think on a relative basis to its peer group and to its cash-generating power and the quality of its cash-generating power, it's certainly very inexpensive compared to its peer group. We've seen very, very strong growth, which can be transformative, which can be exceptional. Yet, at the same point, that is anchored by strong cash-flow and a strong financial position. I see a fairly moderately low risk inexpensive story that has exponential growth potential through organic growth.

Dr. Allen Alper: Great reasons our high-net-worth readers/investors should look closely at Sierra Metals. Is there anything else you'd like to add?

Mr. Mark Brennan: We've come out of the restructuring at Yauricocha at the end of the second quarter. I think we're going to see an exceptional third quarter. I think we're going to see continued growth as we move forward. As of yet I don't think that's been widely recognized. I think it has been recognized in certain respects, but not yet widely. I think we have lots of potential for growth here.

Dr. Allen Alper: That sounds excellent.

http://www.sierrametals.com/

Investor Relations

Mike McAllister

Sierra Metals Inc.

T +1 866 493 9646

info@sierrametals.com

|

|