Earlier this year I documented

seasonal moves in the prices of gold and oil over the past 20 years, copper over

13 years, and the Toronto Venture Exchange Index over 14 years (Mercenary Musings:

January 4

;

March 28

;

April 11

;

June 13

).

I now present our research on

the seasonality of the Baltic Dry Index (BDI). In this case, we obtained data from 2003 to 2016. In a series of

normalized charts, we will show that for bull, bear, and overall market

conditions, there are predictable intra-year trends in the value of the Baltic

Dry Index.

Many lay investors may not be

familiar with the Baltic Dry Index; therefore, I offer a brief explanation:

The BDI measures the current

price of moving raw materials by sea. It is posted five days a week, exclusive

of holidays and from Xmas until the first work day of the New Year.

The Index is compiled and

posted by the Baltic Exchange of London and covers four different sizes of bulk

cargo ships on 23 shipping routes throughout the world.

The Baltic Exchange has a

long history. It was founded in 1744 by a group of merchants and traders in a London

coffee house and called the “Virginia and Baltick”, reflecting England’s major

sources of international commerce at the time. By 1823, it consisted of a

merchant committee that regulated trade and operated a securities exchange from

a local tavern. It admitted the London Shipping Exchange as a member in 1900

and organized as a private limited company with shareholders. In 1992, its

iconic building was destroyed by an Irish Republican Army bomb. In early

November of this year, the Baltic Exchange was acquired by the Singapore

Exchange in a friendly transaction.

The Exchange consists of over

600 member firms and is the world’s only source of maritime market information for

the trading and settlement of physical and derivative shipping contracts.

The Baltic Dry Index was

started in 1985 and surveys a panel of international shippers on a daily basis

for assessments of rates. It is a weighted index that considers shipping routes

and volumes for the four different categories of cargo ships. BDI covers 100%

of bulk dry cargo in transit on the world’s oceans but does not include ships

transporting freight via container or transport of energy liquids by tanker.

The largest bulk cargo ships

carry over 100,000 dead weight tonnes and are called “Capesize” because they

are too large to enter the Panama or Suez Canals; i.e., they must travel around

the southern capes of South America and Africa. These ships, which can reach up

to 400,000 tonnes capacity in Southeast Asia, handle 62% of the world’s bulk

dry cargo, mostly iron ore and coal.

Other sizes of bulk dry cargo

ships include: Panamax, which carry from 60,000 to 80,000 dead weight tonnes,

and handle about 20% of world cargo; Supramax from 45,000 to 59,000 tonnes, and

Handysize from 15,000 to 35,000 tonnes. The latter two carry of 18% of annual

world cargo.

BDI is a direct measure of

the supply of dry bulk carriers versus demand for shipping capacity. The supply

part of the equation, consisting of about 9000 vessels worldwide, is tight and

inflexible. Unlike oil tankers, it is costly to park and idle a cargo ship, and

new ships take two years to build. Because of fluctuating world and regional demand,

the Index can be wildly volatile on both the upside and downside.

The Index indirectly measures

global supply and demand for metallic ores, coal, grains, steel, and industrial

and agricultural minerals. Because 95% of the metal mined worldwide is iron ore,

the Index is dominated by this commodity. Coal (both coking and thermal) is the

second most important material contributing to the Index. Copper and bauxite are

other metallic ores of consequence; steel, timber, and cement are important

construction materials.

BDI is a “leading economic indicator”

in that it measures the transportation cost of raw materials used for production

of finished goods. Therefore, it is an important input in predicting short-term

economic activity.

There is no speculative

component in the Baltic Dry Index because freighters are contracted only if

there is cargo to move. That said, there is a freight derivatives market

operated by the Baltic Exchange and administered by brokers that allows principals

and traders to lock-in or hedge freight rates via futures contracts. These

derivatives are collectively called “forward freight agreements”.

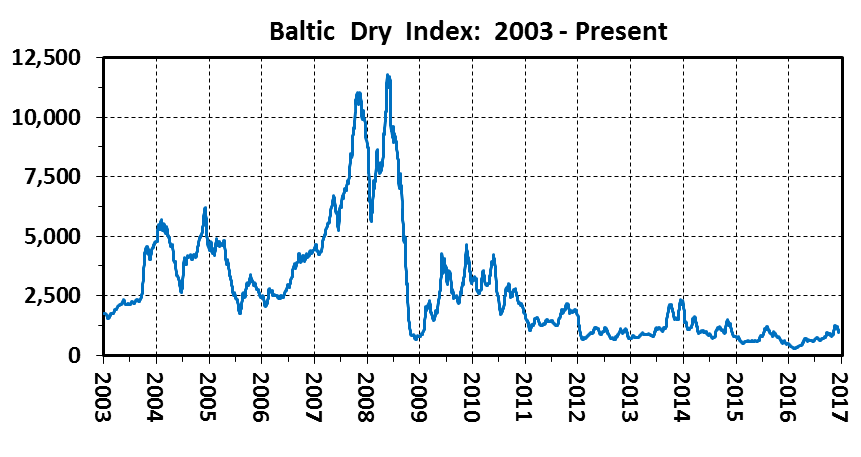

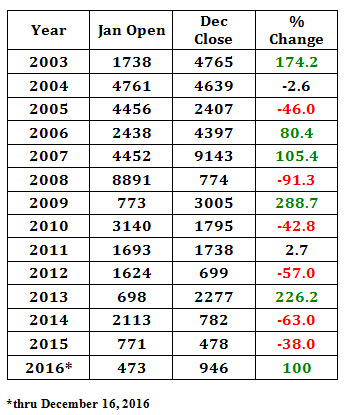

This is the daily record of

the BDI from the beginning of 2003 thru December 16, 2016:

The Baltic Dry Index has

exhibited extreme volatility over the past 14 years with rises and falls

broadly corresponding to bull and bear markets for industrial commodities.

BDI’s all-time high of 11,793

was reached on May 20, 2008 in the second of two parabolic spikes when

commodity prices peaked. By December 5 of that year, it had plunged to a

post-1986 low of 663 for a 94% decline as commodities demand crashed amid the

global economic crisis.

From early 2012 to Q3 2016, a

deep bear market for commodities resulted in the Index trading well-below its

previous low. Its all-time bottom of 290 occurred on February 11 of this year

due to severely depressed demand for iron ore and coal and a glut of carriers.

Since that time, BDI has

moved sharply upward as the commodities sector enters an incipient bull market

cycle. It reached 1257 on November 18 but is currently trading in the mid-900 range

as cargo shipping reaches its usual year-end lull. The 25% decline over the

past month attests to the Index’s volatility.

Economic factors that

influence movements of the BDI include:

-

·

Supply, demand, and

prices of bulk dry commodities.

-

·

Vessel supply and

capacity.

-

·

Crude oil prices

and the resulting cost of bunker fuel.

-

·

Seasonality in

the transport of commodities.

-

·

Port congestion

and choke points including straights, channels, and canals.

-

·

Health of the

world’s economy and overall market sentiment.

-

·

Geopolitical events,

labor issues, weather, and accidents in exporting and importing countries.

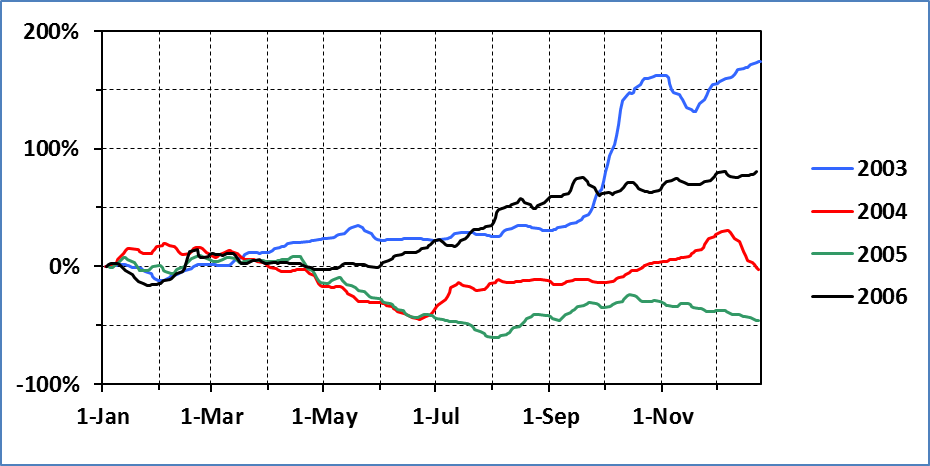

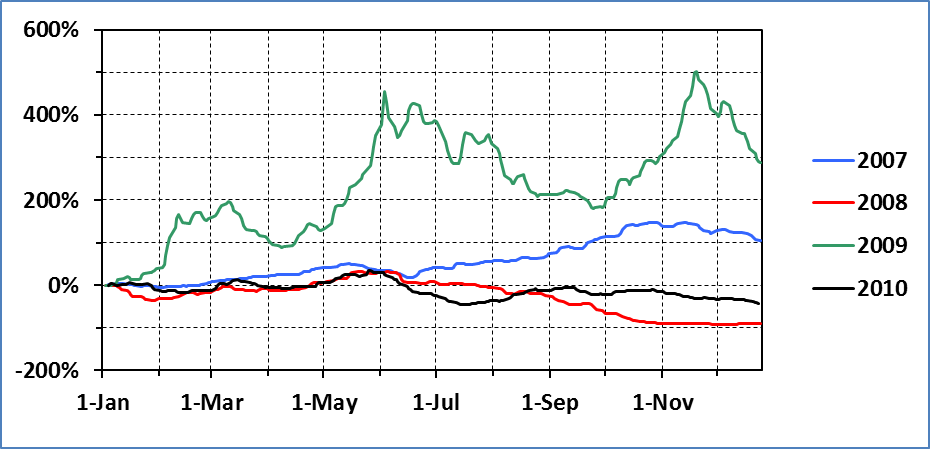

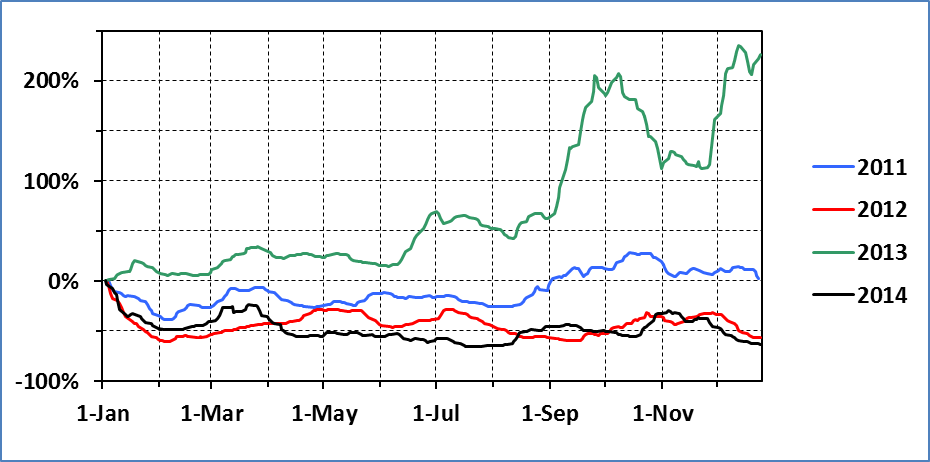

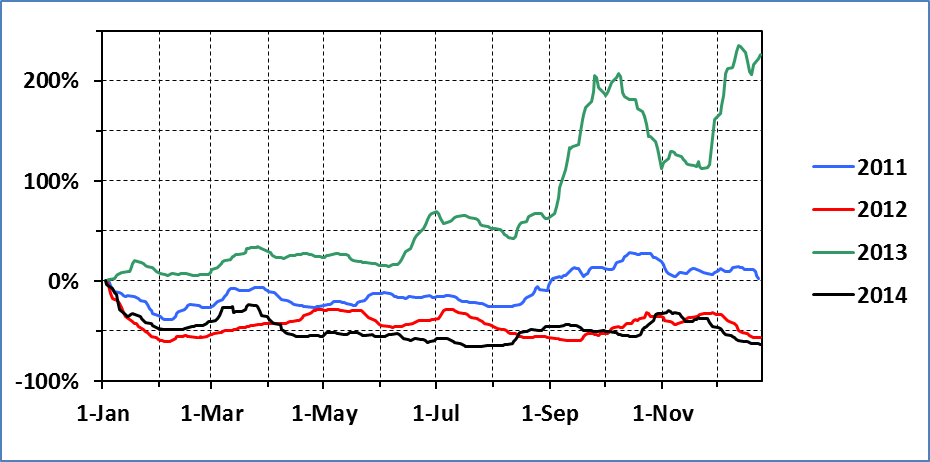

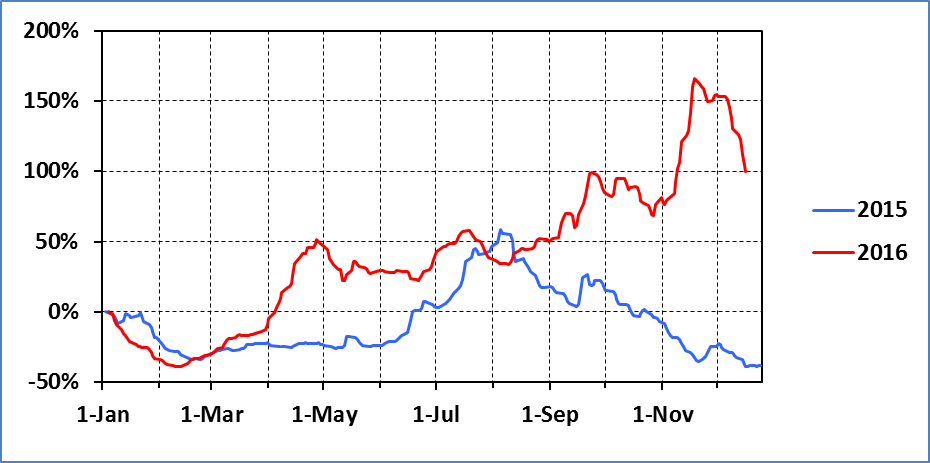

The following series of four charts

shows percent change in the daily value of the Baltic Dry Index normalized to

January 1 for each year:

Based on annual opening and

closing values, we define bull market years for the Baltic Dry Index (green)

as those in which the price closed the year > 10% higher than it opened;

bear market years (red) as those in which the price closed the year

>10% lower than it opened; and neutral years (black) as those in which the percentage change was less than 10%:

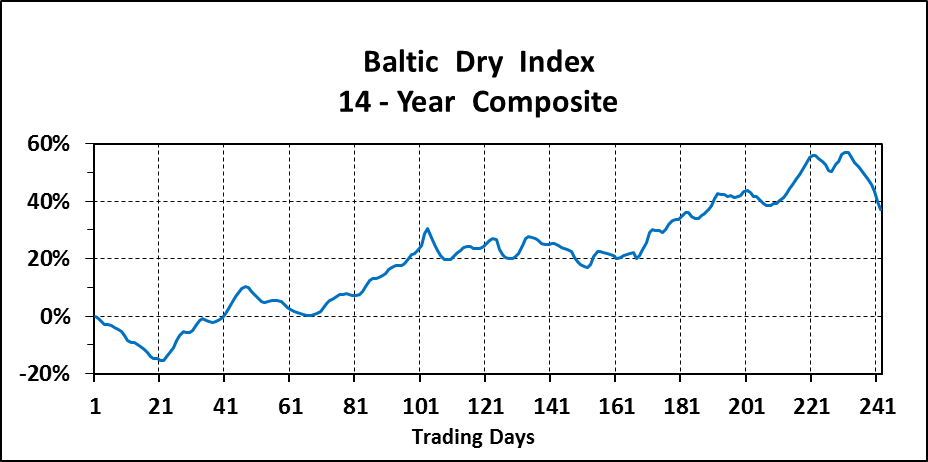

The Baltic Dry Index has an

average range from the beginning to end of a given year of 94% over the past 14

years.

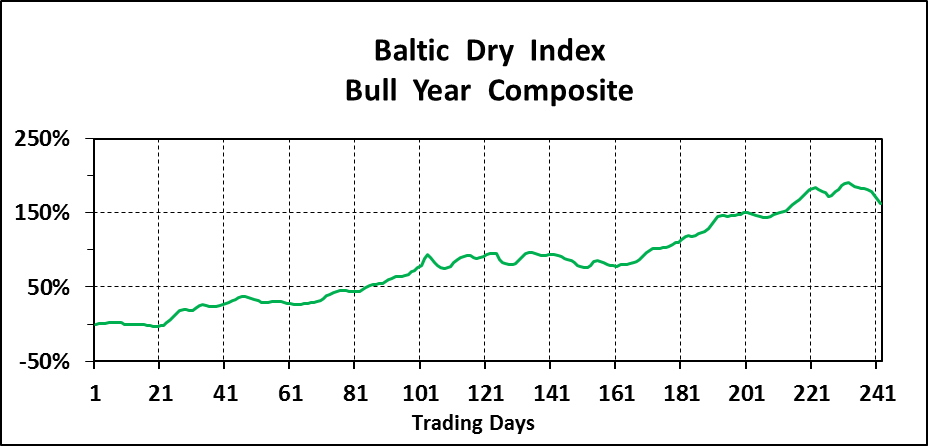

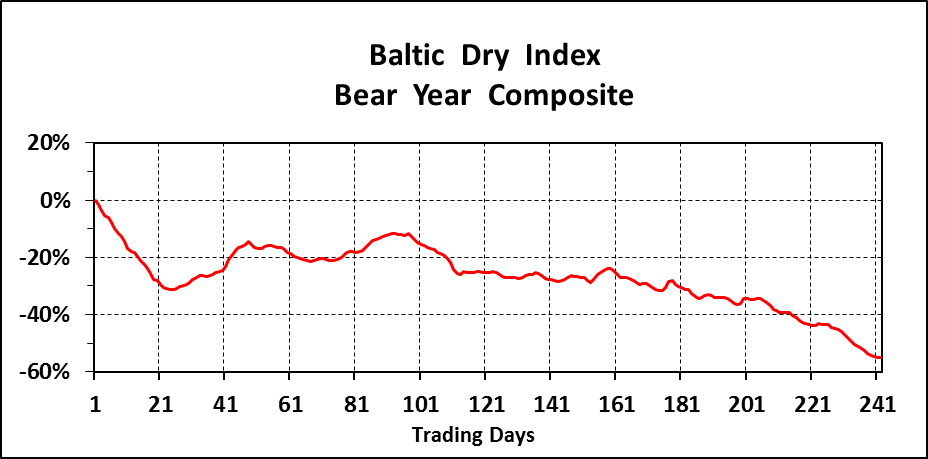

The following three charts

present composite yearly trends from January 1 to December 24 for the entire 14-year

period, six bear years (2005; 2008; 2010; 2012; 2014-2015), and six bull years

(2003; 2006-2007; 2009; 2013; 2016).

We have chosen to disregard

the two neutral years (2004; 2011) as a separate data set because of small

sample size.

Please note the significant change

in y-axis scale for the bull years; its data range is 200% as opposed to 75%

for the overall composite and 55% for bear years:

The composite charts

illustrate interesting seasonal trends for the Baltic Dry Index:

-

·

There is a

general fall in the BDI Index from the beginning of January to early February.

It is prominent in the composite and the bear market years while in bull market

conditions, the Index is flat during this period.

-

·

The Index rallies

robustly from early February to early March and then falls off from mid-March

to mid-April regardless of market trend.

-

·

BDI rises in a

steady manner from mid-April until late May (bear market years) or early June

(bull and overall market years).

-

·

In bear years,

the Baltic Dry Index undergoes a steep decline from late May thru mid-June and

then steadies during the early summer. Beginning in late July it undergoes a

steady downtick for the remainder of the year.

-

·

For overall and

bull market composites, the BDI is flat and oscillating during the summer

months. Then it goes mostly higher from mid-September thru early December,

except for a pause in late October to mid-November.

-

·

In all cases,

there is a significant drop-off in the Baltic Dry Index during the second and

third weeks of December. The BDI is not posted from Christmas thru New Year’s.

Now

let’s explore some factors that can account for the well-defined seasonal

trends in the Baltic Dry Index:

-

·

The early January

to early February fall is attributable to wintertime shuttering of some mine

operations and ports and the Chinese New Year when that country shuts down for

about two weeks.

-

·

A rally occurs over

the next month as economic activity in China resumes.

-

·

The mid-April to

early May rise in BDI is likely caused by building of inventories in copper,

timber, steel, and cement in anticipation of peak Northern Hemisphere

construction season.

-

·

In addition, bunker

fuel is costlier in the spring when crude oil prices generally rise as American

refineries ramp up for summer driving season.

-

·

BDI is flat

during the summer months while construction activity uses stockpiled materials.

-

·

Rates tend to

rise from mid-September to late October when grain harvests are shipped and

customers re-stock commodities (especially steel-making materials and thermal

coal) in advance of the Northern Hemisphere winter.

-

·

A lull then occurs

before rates generally move upward again from mid-November thru early December

when China imports more iron ore from Australia and Brazil in advance of their wet

seasons.

-

·

Freight rates drop

as economic activity winds down in North America and Europe in mid- December.

Our research indicates there

is a pronounced seasonality in the Baltic Dry Index over the14 years of

available daily history. This documented seasonality reflects current supply and

demand conditions for the world’s most important metallic, industrial, and

agricultural commodities transported in bulk by cargo ships.

The Index is a leading

economic indicator because it is a predictor of the total cost of raw materials

delivered to customers who produce manufactured goods and pass costs on to

wholesale buyers and then to retail consumers.

The Baltic Dry Index is an

important input that I use to forecast short-term commodity price movements and

macroeconomic trends.

Ciao for now,

Mickey Fulp

Mercenary Geologist

Acknowledgment:

Troy

McIntyre is the research assistant for

MercenaryGeologist.com

.

The

Mercenary

Geologist Michael S. “Mickey” Fulp

is a Certified Professional

Geologist

with a

B.Sc. Earth Sciences with honor from the University of Tulsa, and M.Sc. Geology

from the University of New Mexico. Mickey has 35 years experience as an

exploration geologist and analyst searching for economic deposits of base and

precious metals, industrial minerals, uranium, coal, oil and gas, and water in

North and South America, Europe, and Asia

.

Mickey worked for junior explorers, major

mining companies, private companies, and investors as a consulting economic

geologist for over 20 years, specializing in geological mapping, property

evaluation, and business development. In

addition to Mickey’s professional credentials and experience, he is

high-altitude proficient, and is bilingual in English and Spanish. From 2003 to

2006, he made four outcrop ore discoveries in Peru, Nevada, Chile, and British

Columbia.

Mickey is well-known and highly respected throughout

the mining and exploration community due to his ongoing work as an analyst, writer,

and speaker.

Contact

:

Contact@MercenaryGeologist.com

Disclaimer

and Notice

: I am not a

certified financial analyst, broker, or professional qualified to offer

investment advice. Nothing in any report, commentary, this website, interview,

and other content constitutes or can be construed as investment advice or an

offer or solicitation or advice to buy or sell stock or any asset or

investment. All of my presentations should be considered an opinion and my

opinions may be based upon information obtained from research of public documents

and content available on the company’s website, regulatory filings, various

stock exchange websites, and stock information services, through discussions

with company representatives, agents, other professionals and investors, and

field visits. My opinions are based upon information believed to be accurate

and reliable, but my opinions are not guaranteed or implied to be so. The

opinions presented may not be complete or correct; all information is provided

without any legal responsibility or obligation to provide future updates. I

accept no responsibility and no liability, whatsoever, for any direct,

indirect, special, punitive, or consequential damages or loss arising from the

use of my opinions or information. The information contained in a report, commentary,

this website, interview, and other content is subject to change without notice,

may become outdated, and may not be updated. A report, commentary, this

website, interview, and other content reflect my personal opinions and views

and nothing more. All content of this website is subject to international

copyright protection and no part or portion of this website, report,

commentary, interview, and other content may be altered, reproduced, copied,

emailed, faxed, or distributed in any form without the express written consent

of Michael S. (Mickey) Fulp, MercenaryGeologist.com LLC.

Copyright © 2016

Mercenary Geologist.com, LLC. All Rights Reserved.