Adrian

Day likes to think long term, and historical trends persuade him that the bull

market in gold should continue for years to come. In this interview with The Gold Report, the founder of Adrian

Day Asset Management explains why he expects a significant gold price recovery

in the near future. In the short term, he counsels investors to choose

companies that minimize risk through royalty agreements, joint ventures and

robust balance sheets. In other words, companies with the means to seize

profit-making opportunities, and Day shares the names of a handful that fit the

bill

Adrian

Day likes to think long term, and historical trends persuade him that the bull

market in gold should continue for years to come. In this interview with The Gold Report, the founder of Adrian

Day Asset Management explains why he expects a significant gold price recovery

in the near future. In the short term, he counsels investors to choose

companies that minimize risk through royalty agreements, joint ventures and

robust balance sheets. In other words, companies with the means to seize

profit-making opportunities, and Day shares the names of a handful that fit the

bill

The Gold Report: John Makin of the American Enterprise

Institute noted on Dec. 20, "In 2013, the Federal Reserve's

actual monthly purchase of bonds—the size of quantitative easing (QE)—has

averaged $94 billion ($94B), or $9B above the advertised pace of

$85B/month." So is all this talk of tapering a shell game?

Adrian Day: Even if the Fed had stuck to the

$85B/month as advertised, tapering is a sham. The Fed reduced QE to $75B/month

in January and now has announced a further $10B/month reduction. But $65B/month

is still an enormous amount of stimulus. Very shortly, the Fed's balance sheet

will exceed $4 trillion. We're focused on the wrong thing here.

TGR: Considering all this talk of recovery,

the Jan. 10 jobs report was dismal, was it not?

AD: Absolutely. The employment situation in

the U.S. is a long way from what one would expect from a decent recovery, let

alone a robust recovery.

TGR: U.S. job creation since 2008 has been

mostly part-time jobs, temporary jobs and low-paying jobs. How does this lead

to increased consumer spending, which is, we are told, the basis of a robust recovery?

AD: Consumer spending is

being fuelled by debt. Since 2007, it has increased 23% for the lower 40% of

earners. The Fed reports that net household income and net household wealth

have now exceeded the 2007 highs. If we break down the numbers, however, we see

that net worth is actually down for 90% of U.S. households. For the bottom 50%

of households, net worth is down an astonishing 44%.

TGR: We can't have a recovery based on the purchase of yachts and multimillion-dollar New York City condos, can we?

AD: Of course not. We can't have a strong

economy based on just 10% of the population getting richer. Frankly, I don't

mind whether there's a gap between the rich and the poor—so long as the rich

are getting their wealth honestly and not from government handouts. And so long

as the middle class is getting richer also.

TGR: President Kennedy said famously that a

rising tide lifts all boats. Do we still believe that?

AD: Since 2008, the Fed's stimulus has gone

mostly to Wall Street, not to Main Street. That is a fundamental problem for

the economy but also for the polis, for the public social good.

It's not that I want

the government to do things specifically for the middle class; I just want it

to get out of the way. If small businesses are created and can expand and hire

people, then we will have a rising tide lifting all boats.

TGR: The International Monetary Fund last

month cautioned that debt levels have become so perilous that

recovery, as Ambrose Evans-Pritchard of The Daily Telegraph wrote, "will require defaults, a savings tax and higher

inflation." Do you agree?

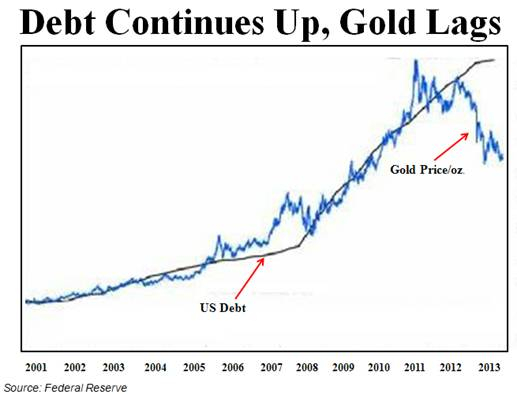

AD: Debt has become unmanageable. Now, there

is nothing wrong with debt per se. When I argue against high government debt,

people often respond that in the 19th century the U.S. debt to GDP ratio was

higher than today. But that debt was used for capital investment (canals,

railroads, etc.), which led to higher economic growth. Today, debt is being

used to fund wars and welfare, not investments in the future.

Defaults? Perhaps.

Taxes will never deal with the debt problem. You could tax 100% of income above

$100,000, and you would fix the U.S. deficit only for a few months. Higher

inflation? Perhaps. The one thing Evans-Pritchard didn't mention was currency

devaluation. Because the vast majority of U.S. debt is issued in U.S. dollars,

the easiest way to liquidate it is to devalue the dollar.

TGR: In a speech last month in Shanghai, you said,

"Gold moves in long cycles." Do all commodities move in cycles?

AD: Most do because producers get price

signals from the market with a delay. Take the retailer that sells TVs. If

sales go down three weeks in a row, the retailer will order fewer units the

next month. He gets an immediate price signal. The wholesaler gets signals with

a bit of a lag but still relatively early.

But the producer of a

rare earth that goes into TVs gets the signal from the market with a much

longer lag than the retailer, the wholesaler and the manufacturer. So, metals

cycles tend to be very long. And it's far more difficult for miners to cut back

or increase production than for retailers to adjust orders.

TGR: Where are we in the current gold cycle?

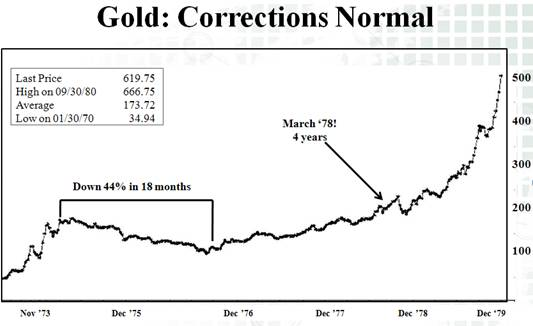

AD: Over the last 250 years, the shortest

cycle on record was the 1970s, just over 10 years. Typically, gold upcycles

have lasted close to 40 years. On that basis, we aren't even halfway through

the current gold upcycle.

TGR: So last year's price collapse did not

indicate the end of the gold upcycle?

AD: Significant corrections in long, secular

bull markets are typical. Gold, from top to bottom, has declined 37% in this

particular cycle. If you look back to the upcycle of the 1970s, 1975–1976 saw a

midcycle correction of 47%. But that was right before gold went up eightfold to

more than $800/ounce ($800/oz).

Where are we now? It

would be optimistic to assume a V-shaped recovery, but gold has bottomed, and

over the next 12 months we are likely to see a slow, if uneven, recovery. The

typical recovery comes from a long midcycle correction. We should reach

$1,550–1,650/oz in 2014 or early next year, and then gold will start to

accelerate. Some gold stocks could recover a lot quicker in expectation of

higher prices.

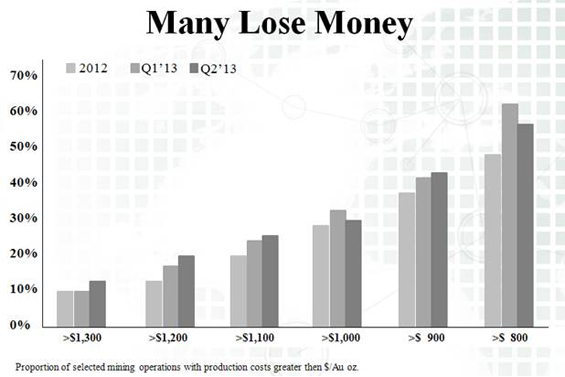

TGR: You noted in Shanghai that gold stocks

have lagged behind the gold price in an extraordinary manner. Why?

AD: First, costs have gone up, in some cases

more dramatically the price of gold. Second, companies grossly overpaid for

acquisitions with no synergies. Barrick Gold Corp. (ABX:TSX; ABX:NYSE) comes to

mind in this regard.

For these reasons, we've

seen a great deal of new equity dilution. If we look at all-in costs—and not

just mining costs— it's been estimated that about half of all mines are losing

money. So it's no surprise that gold stocks have done badly, particularly in

light of the attractive and simple alternative: gold exchange-traded funds.

TGR: When can we expect gold stocks to

recover?

AD: As you know, many gold companies have made big

mea culpas. They've fired CEOs and committed to not making the same mistakes.

The irony is that with companies and individual mines so cheap now, when it's

so difficult for companies to raise capital, this is precisely when the big

companies should be making acquisitions.

That's why I

applaud Goldcorp Inc.'s

(G:TSX; GG:NYSE) bid for Osisko Mining Corp. (OSK:TSX). I think

a few more mergers and acquisitions (M&A) like this will get the market

excited again.

TGR: Assuming a general recovery in gold

stocks, which sector do you think will do best—majors, mid-caps or micro-caps?

AD: Broadly, the seniors will probably move

first because when generalist investors move into the gold sector, that's

typically where they first put their money.

But I don't look at

the gold sector that way. Today, the most important criterion is the balance

sheet. Does the company have the cash to carry out its plans? If it must raise

cash, can it do so in a nondilutive manner? Some seniors will be able to answer

affirmatively, and so will some explorers. That's the test.

TGR: It's said that some companies are too

big to fail. Are some gold companies, like Barrick, too big to succeed?

AD: There's no systemic reason why Barrick

is too big to succeed. It has a complex and far-flung structure, but so does

Nestlé S.A., which buys from more than 100 countries and sells to more than

200. Nobody says that Nestlé is too big to succeed. Barrick's problem is that

it probably grew too big too fast.

Successful exploration

entails risks and the understanding most risks will fail. It's natural that

lower-level managers in large companies become much more risk averse. The

solution is for the majors to use the juniors as their exploration arm, as

companies like Newmont Mining Corp. (NEM:NYSE) have done. Newmont does

joint ventures (JVs) with other companies and then, if appropriate, buys the

properties or buys its partners outright.

TGR: How long until Barrick's new management

can put its stamp on the company and tell investors: That was then, and this is

now?

AD: The first thing Barrick must do is make

it very clear exactly what kind of company it is: does it want to be a gold

company or a diversified mining company? Will it hedge? Considering the way the

management transition has been handled—the $11.9 million ($11.9M) signing bonus

for new Co-chairman John Thornton and the two independent directors resigning

because they think the "independent" directors are still too close to

Peter Munk—I think it's going to be a while before Barrick can draw a line

under the past.

TGR: Why do you favor the royalty/streaming

model?

AD: When a company acquires or creates a

royalty on another company, that first dollar in is typically the last dollar

in, meaning that the royalty company is not responsible for setbacks. If there

are cost overruns, if the shaft floods, if taxes are raised, the company with

the royalty is not responsible.

The worst that can

happen is that royalty payments are reduced or delayed. For instance, the

original capital expenditure (capex) of Pascua Lama, Barrick's project that

straddles Chile and Argentina, was $2.25B. By the time it was shelved, the

capex had reached $10B.Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX), which had a royalty on

Pascua Lama, was not responsible for this huge increase. Of course, Royal still

doesn't have any revenue from that project, but at least it didn't have to

front any more money.

TGR: What are the advantages for royalty

companies besides risk mitigation?

AD: Staffs tend to be small, so profit

margins tend to be high. And royalty companies have exposure to exploration

upside. If a company has a royalty on a particular mine, it will typically have

a royalty on at least some of the exploration ground around that mine. If there

is a discovery on that ground, the royalty owner benefits just as much as if it

were the company making the discovery. Royalty companies get most of the upside

and very little of the downside.

TGR: Which royalty companies do you like?

AD: I like most of them. Having said

that, Franco-Nevada Corp.

(FNV:TSX; FNV:NYSE) is, in my view, far and away the best. It

has great management, a great balance sheet, about $900M in cash and no debt.

It has a very broad portfolio of properties. It has royalties on 37 producing

mines and more than 300 other, nonproducing royalties.

TGR: Which of the smaller royalty companies

do you like?

AD: It's not in the gold business, but Altius Minerals

Corp. (ALS:TSX.V) has morphed into a royalty company. It began

as a low-risk operation, partnering on JVs. It then innovated by spinning off

projects but retaining shares and royalties.

Altius has just

acquired a package of royalties on coal and potash. Add that to its royalties

on Vale S.A.'s (VALE:NYSE) Voisey's Bay nickel mine and Alderon Iron Ore

Corp.'s (ADV:TSX; AXX:NYSE.MKT) developmental Kami iron ore project in

Newfoundland and you have a very attractive company.

I also like Virginia Mines

Inc. (VGQ:TSX), which, like Altius, has grown largely with JVs. It

has a royalty on Éléonore in Quebec, which is Goldcorp's next major mine to

come onstream, in Q4/14. Production is estimated at 600,000 oz annually after

ramp up.

TGR: Your January portfolio review noted that

Altius was up 24% for 2013, and Virginia Mines was up 16%.

AD: Most of the mining companies that did

well last year had very good balance sheets and weren't associated with high

risk. That's certainly true of Altius and Virginia.

It amazed me that

Virginia was still so inexpensive even as Éléonore's net present value

continued to grow and Virginia's royalty came ever closer to fruition. The

explanation is that investors are short-term oriented. Virginia is arguably a

little ahead of itself after the recent run, given today's gold price, but it

is still one of the top companies I would want to hold long term.

TGR: Any other royalty companies you'd care

to mention?

AD: Callinan

Royalties Corp. (CAA:TSX.V). Again, it's not gold. Callinan actually

pays a dividend, about 4.6%. It's quite nice to get a decent dividend on a

resource-related company. Callinan has a good balance sheet and is continuing

to make investments in other companies where it retains royalties. Over the

next few years, investors will see Callinan expand from basically one producing

royalty to several. In the meantime, investors get paid.

TGR: Reservoir

Minerals Inc. (RMC:TSX.V) was up 21% last year. What's its

story?

AD: Reservoir has a JV with Freeport-McMoRan

Copper & Gold Inc. (FCX:NYSE) on the Timok copper-gold project in Serbia.

This proves again the worth of the JV model. Reservoir had to give up 75% of

Timok, but with Freeport paying for the exploration, Reservoir can maintain its

balance sheet.

Reservoir has about

$18M in cash right now, which is a lot, considering what its expenditures are.

It has had continually spectacular results from Timok. I think that Freeport is

going to buy Reservoir or, at least, buy Timok. This could mean a very

significant premium over the current stock price. Most shareholders are waiting

for the endgame, so there aren't a lot of shares available. So it's important

to look for any setback to buy, and to use a limit.

TGR: Moving to British Columbia's biggest

exploration story, could you explain the "battle of the consultants"

over the quality of Pretium Resources Inc.'s (PVG:TSX; PVG:NYSE) Brucejack

deposit?

AD: That was unfortunate. Pretium had two

independent consultants, Strathcona and Snowden. Strathcona is the company that

blew the whistle on Bre-X, so it has credibility. Pretium was doing a bulk

sample to assess the value of Brucejack because the deposit is high-grade but

spotty. The two companies had different methodologies for conducting and

assessing this sample. These were technical differences, and I don't know why

Strathcona believed it had to resign from the project so publicly.

TGR: You sold Pretium, but now you're bullish

on it again.

AD: We sold because I was in a risk-averse

mode at the time. I know Pretium's CEO, Bob Quartermain, and his integrity is

unquestioned. Nonetheless, I knew that a very public controversy like this

would cause the stock to decline for quite some time, which it did.

Then the initial bulk

sample results were released, and they were excellent. So I thought it was time

to jump back in. I feel very positive about the deposit, and the bulk sample

results have only gone to support that confidence. I think Pretium is a good

buy at this point.

TGR: You have stressed the correlation of

success with cash and/or cash flow. Name a company that demonstrates these

attributes.

AD: Almaden Minerals

Ltd. (AMM:TSX; AAU:NYSE) has great management, about $16M in

cash plus a couple of million in gold bullion. The beauty of having cash means

that a company can raise money or sell assets only when it wants to.

Almaden owns the

Tuligtic gold-silver property in Puebla, Mexico. The company continues to drill

the Ixtaca zone aggressively, and the results continue to be strong. A

just-released updated resource estimate on the Ixtaca zone on this project

shows an increase in total resource of about 20% and a Measured and Indicated

resource of 3.5 million ounces; the deposit continues to grow. A preliminary

economic assessment is scheduled for early March and I am expecting it to be

positive. This stock is a bargain.

TGR: Any other bargains come to mind?

AD: Midland

Exploration Inc. (MD:TSX.V), another prospect generator. It has 10

main projects in Quebec, five of which are currently under joint venture. Key

projects are the Maritime-Cadillac gold project with Agnico-Eagle Mines Ltd.

(AEM:TSX; AEM:NYSE), the Patris gold project with Teck Resources Ltd. (TCK:TSX;

TCK:NYSE) and the Ytterby rare earth project with Japan Oil, Gas and Metals

National Corp. (JOGMEC). These partners have already re-upped, which

demonstrates confidence in the projects, and the company is working on finding

partners for more of its projects. Midland has $4.5M in cash, more than enough,

considering the money its partners are spending.

Midland's stock is at

$0.97/share. It's a very thinly traded company, so I would urge investors to

use a limit price when they buy, otherwise they'll just push the price up on

themselves. (Our clients actually own more than 10% of Midland, and we're

considered an insider.)

TGR: Could you rate the balance sheets of

some other gold companies?

AD: We own Detour Gold

Corp. (DGC:TSX). It does have cash, but it also has ongoing capital

expenditures on its Detour Lake mine in Ontario. It's more leveraged on the

gold price than some of the other companies I've mentioned. If gold goes from

$1,200 to $900/oz, it's not going to be a great investment. But if gold goes

from $1,200 to $1,500 or $1,600/oz, Detour will be one of the better

performers. It is also a potential takeover candidate.

We also own quite a

bit of New Gold Inc.

(NGD:TSX; NGD:NYSE.MKT). It has four producing mines: Cerro San

Pedro in Mexico, Mesquite in California, New Afton in British Columbia and Peak

in Australia. It also has very strong management. Randall Oliphant, the

executive chairman, is a former Barrick CEO, and board member Pierre Lassonde

is chairman of Franco-Nevada.

New Gold has a good

balance sheet and a good pipeline of projects. It is one of the most

undervalued of the senior gold companies. So I would definitely be a buyer

there.

TGR: Adrian, thank you for your time and your

insights.

Adrian Day,

London born and a graduate of the London School of Economics, heads the

eponymous money management firm Adrian Day Asset Management (www.adriandayassetmanagement.com;

410-224-2037), where he manages discretionary accounts in both global and

resource areas. Day is also sub-adviser to the new EuroPacific Gold Fund

(EPGFX). His latest book is "Investing in Resources: How to Profit from

the Outsized Potential and Avoid the Risks."

Want to read

more Gold Report interviews like this? Sign up for

our free e-newsletter, and you'll learn when new articles have been published.

To see a list of recent interviews with industry analysts and commentators,

visit our Streetwise Interviews page.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Gold Report and

provides services to The Gold Report as an independent

contractor. He or his family own shares of the following companies mentioned in

this interview: None.

2) The following companies mentioned in the interview are sponsors of The

Gold Report: Virginia Mines Inc., Pretium Resources Inc., Almaden

Minerals Ltd. and Midland Exploration Inc. Goldcorp Inc. and Franco-Nevada

Corp. are not affiliated with The Gold Report. Streetwise

Reports does not accept stock in exchange for its services or as sponsorship

payment.

3) Adrian Day: I or my family own shares of the following companies mentioned

in this interview: Almaden Minerals Ltd., Altius Minerals Corp., Franco-Nevada

Corp., Freeport-McMoRan Copper & Gold Inc., Goldcorp Inc., Midland

Exploration Inc., Reservoir Minerals Inc., Royal Gold Inc. and Virginia Mines

Inc. I personally am or my family is paid by the following companies mentioned

in this interview: None. My company has a financial relationship with the

following companies mentioned in this interview: None. I was not paid by

Streetwise Reports for participating in this interview. Comments and opinions

expressed are my own comments and opinions. I had the opportunity to review the

interview for accuracy as of the date of the interview and am responsible for

the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make

editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is

encouraged to consult with his or her individual financial professional and any

action a reader takes as a result of information presented here is his or her

own responsibility. By opening this page, each reader accepts and agrees to

Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers,

employees or members of their families, as well as persons interviewed for

articles and interviews on the site, may have a long or short position in

securities mentioned and may make purchases and/or sales of those securities in

the open market or otherwise.

Streetwise

- The Gold Report is Copyright © 2014 by

Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby

grants an unrestricted license to use or disseminate this copyrighted material

(i) only in whole (and always including this disclaimer), but (ii) never in

part.

Streetwise

Reports LLC does not guarantee the accuracy or thoroughness of the information

reported.

Streetwise

Reports LLC receives a fee from companies that are listed on the home page in

the In This Issue section. Their sponsor pages may be considered advertising

for the purposes of 18 U.S.C. 1734.

Participating

companies provide the logos used in The

Gold Report. These logos are trademarks and are the property of the

individual companies.

101

Second St., Suite 110

Petaluma, CA 94952

Tel.:

(707) 981-8999

Fax: (707) 981-8998

Email: jluther@streetwisereports.com