Dr. Michael Anderson, Managing Director, Firefinch Ltd (ASX: FFX) Discusses Developing Morila, World-Class Gold Mine to be 150 – 200k oz pa Gold Producer and Goulamina to be One of the Largest Spodumene Producers

|

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 9/21/2021

We spoke with Dr. Michael Anderson, Managing Director of Firefinch Limited (ASX: FFX) - a Mali-focused, gold miner and lithium developer. Firefinch has an 80% interest in the Morila Gold Mine and it currently owns 100% of the Goulamina Lithium Project. Morila is a world-class, ex-AngloGold/Barrick gold mine, transitioning from a 40kozpa tailings, retreatment operation to 150 – 200k oz pa gold producer. Goulamina is expected to be one of the largest spodumene concentrate operations, supplying ~436ktpa to a Tier 1 off-taker in Ganfeng, the world’s largest lithium producer, by production capacity. Firefinch recently announced plans to demerge the Goulamina Lithium Project and form a new Company, called Leo Lithium Ltd. Firefinch’s shareholders will receive an interest in Leo Lithium.

First gold pour at Morila under Firefinch ownership

Dr. Allen Alper:

This is Dr. Allen Alper, Editor-in-Chief of Metals News, interviewing Michael Anderson, who is the Managing Director of Firefinch, Ltd. Michael, could you give our readers/investors an overview of your Company and what differentiates your Company from others?

Michael Anderson, Managing Director of Firefinch, Ltd.

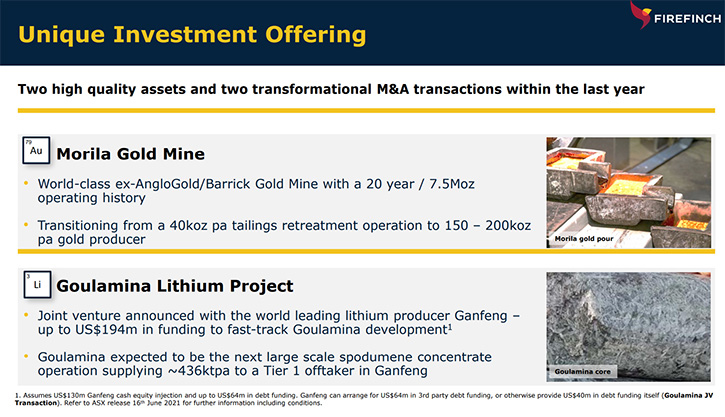

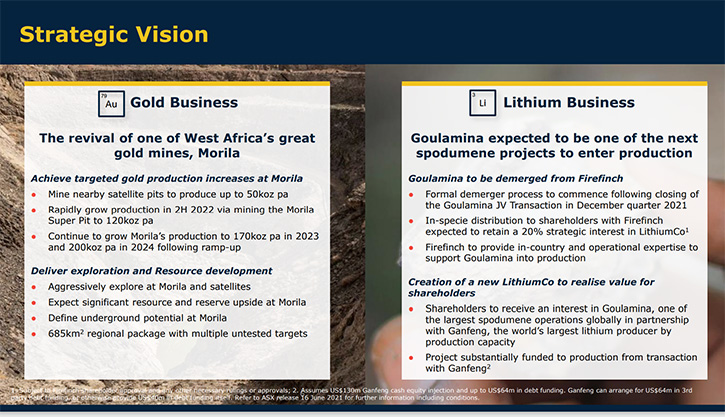

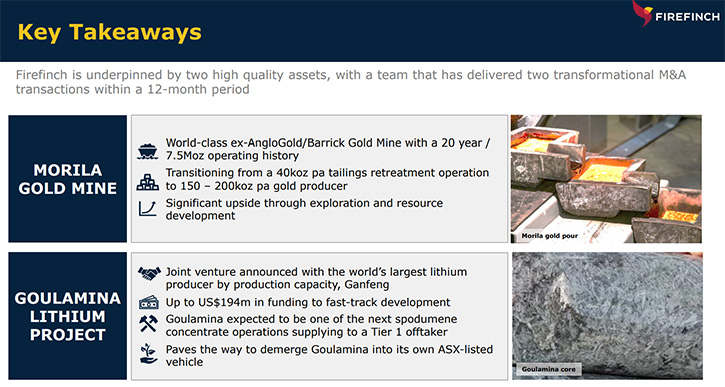

Michael Anderson:Firefinch is focused on Mali, West Africa. We have two assets, The Morila Gold Mine, which we acquired in November of year. Morila had a fantastic history. It produced over 7.5 million ounces in its time. We’re hoping to ramp that mine back up to 200,000 ounces of annual production, in two or three years’ time, once we de-water the Morila Super pit and get back into mining the heart of that ore body.

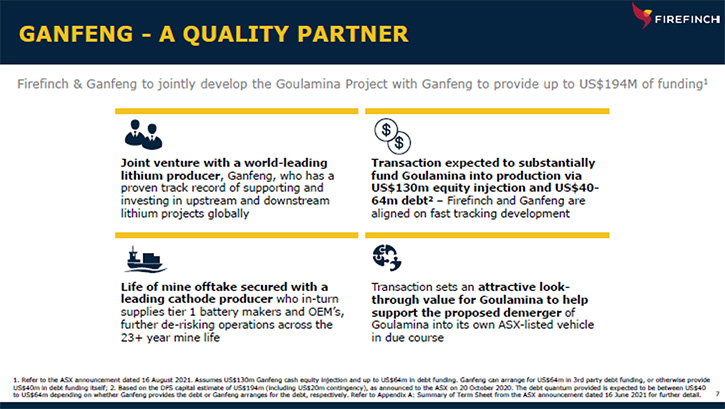

Our second asset is the Goulamina Lithium Project, also in Mali. We recently transacted, with Ganfeng Lithium, out of China, to enter into a joint venture to see that project into development. It will be a 50/50 joint venture, where Ganfeng is bringing the $194 million U.S. of development funding in a combination of equity and debt, which will fund Goulamina into production, hopefully by 2023. So far, so good, in that relationship, we're working together to refresh and update the definitive feasibility study and to progress to hopefully a final investment decision, before the end of the year.

Firefinch’s shareholders will enjoy the distribution, as our plans are to demerge the Goulamina Lithium Project and form a new Company, called Leo Lithium Ltd. We announced that, just over a week ago. It will be an ASX listed Company. We’re looking forward to taking both projects forward and unlocking the significant value that we believe is there and believe that the demerger is the best strategy to do that.

Dr. Allen Alper:

That sounds excellent. Could you tell our readers/investors a little about yourself, your Team and your Board?

Michael Anderson:

We have a pretty experienced Board. I only joined this Company four and a half months ago, in early April, having spent the last 10 years in the asset management business, with Taurus Funds. I was a Managing Director, prior to that, with a Company called Exco Resources. We had a gold project in South Australia and copper projects up in Cloncurry, Queensland, and that connection, with Queensland, was common with our Chairman, Alistair Cowden. He and I were peers, as Managing Directors, back in the mid-2000s, with assets up in that part of the world.

I knew Alistair and during almost a chance conversation, where I was looking at Firefinch, and the Morila asset in particular, with my Taurus hat on, and I wasn't aware that they were looking for a new Managing Director. But once that opportunity was presented to me, I came to the very quick realization of what a fantastic opportunity it was and four months in, no regrets. It's great to be working with Alistair and the rest of the Board.

Brad Gordon, who many would know, used to be the Managing Director of Acacia. He is a very experienced mining engineer, an executive, with lots of experience in gold and a mining engineer by profession. Mark Hepburn, a fellow Director, I've also known for 15, 16 years. He's a very experienced executive in the game. Then Brendan Borg, who probably is more in specialty metals and has a number of very successful Directorships, under his belt in that space. A very experienced Board.

We've recently strengthened our executive team. We've appointed a new CFO, a gentleman by the name of Tom Plant, who has joined us, having spent a long time with Iluka Minerals. We're looking to build this Board and Management Team for the Company that we expect to grow into here. Firefinch has enjoyed a healthy rerate, over the last few months. We're now sitting at a market capitalization of about $550 million Australian. We genuinely believe that both assets, in time, once we achieve steady state production, will be capable of sustaining market caps well in excess of that on their own.

I should also mention, our COO, Andrew Taplin, who spent a long time with Rio in his career, a lot of it in West Africa, too. He has a lot of experience and expertise to chart the course for both of these assets. We are also recruiting for the Executive and Management Team for Leo Lithium and very, very pleased with the caliber of candidates that we're attracting there.

Dr. Allen Alper:

That sounds excellent. That's great to have two outstanding projects, that your stakeholders and shareholders will benefit from, when you spin off the lithium project.

Michael Anderson:

There are a number of precedents, where companies have assets, which are quite different commodities, different metals. There are some very helpful precedents, in fact, Alkane Minerals, with their gold and rare earth assets that they have spun out. And then there's a number of prospective spinoffs that are being discussed, in the assets, at the minute with a similar view. But you do get quite disparate investor groups, who follow gold, and or lithium, etc. And I think this just gives people the ability to make their own choices. They'll end up with two pieces of paper, where they used to have one, and their decision will be whether they hold both one or the other or neither and each to their own. They can make those decisions. But our job is to create the value for them, and we are very focused on doing that.

Dr. Allen Alper:

Oh, that sounds excellent. Could you tell our readers/investors a little bit more about each project, the gold project, and also the lithium project?

Michael Anderson:

Morila began its life back in early 2000. It was the first gold mine that Mark Bristow, who was then with Randgold, had built outside of South Africa, and it had an incredible start. The grades in the heart of Morila, were some of the highest cut grades in the world, at the time, 15, 16 grams per ton average. In its second year or third year, Morila produced over a million ounces. In 2009, they probably had mined the highest-grade portions of the ore body and they were facing the prospect of either a cutback or an underground project.

Morila Gold Mine

With gold prices significantly lower than they are today, I guess they hesitated then and probably had other priorities. Both companies, major companies, had multiple projects to consider. It's not that they shut Morila down, but they did stop mining and they did put the handbrakes on exploration. They did continue with mining and the processing of stockpiles, did a little bit of satellite pit mining. Then, what we inherited last year was a tailings retreatment operation. The facility kept going and was always producing gold. But in its last couple of years, it was only a few tens of thousands of ounces.

When we looked at it, we had a slightly different view from what a major might have. Resources that are around 1.5 grams per ton, and we've already established the guts of 2.5 million ounces, at that grid, with a 1 million ounces reserve. We believe we can make good margins, at current gold prices sitting in the high $1,700. Our modeling suggests that our all-in sustaining cost will be just a touch over $1,100 U.S. and we believe there's some room to reduce those in time. But it's the exploration upside and the near-mined potential, even just below the pit, that's been recently demonstrated.

Our most recent announcement, just last week, at the first hole that we've drilled underneath the high-grade zones at Morila, we intersected 10 meters at 30 grams per ton. It won't take an awful lot more of that to justify a small underground operation, on top of the 7-to-10-year mine life, that we've already defined in the open pit. We have a trajectory here that we'll produce about 50,000 ounces in this calendar year, 2021, as we progress to dewater and pre-strip Morila in the upper benches. We will be on track, for hopefully 120,000 ounces in 2022, 170,000 ounces in 2023 and over 200,000 ounces in 2024. That's before we contemplate any underground potential.

Those sorts of production rates and the types of margins that we hope to be able to achieve, will see us standing alongside a number of peers on the ASX, in particular companies that are producing those sorts of ounces, are already capped at around a billion dollars. That's the gap for us to close, with the path to steady production. A very exciting few years ahead of us here, obviously keeping eyes and ears open for other growth opportunities, be it through organic exploration.

We have a sizable 685 square kilometers of very prospective terrain, at Morila, that we haven't fully tested yet. Moving on to the lithium, Goulamina was the focus for the Company, before we acquired Morila. We completed a feasibility study, mid to late last year, which demonstrated a 23-year mine life with healthy margins, on what was then a price of around $650 dollars a ton. Spot markets at least nearly doubled in recent times. So, clearly a good time to be contemplating bringing a lithium project into production.

We're mindful of our capability as a small company, not only the demerger strategy that was hatched to try and give these assets their own lease on life, but we also felt that it was prudent to enter into some form of joint venture or partnership to help develop the project. We ran what turned out to be a very successful process, beginning in March this year, with Macquarie Bank here in Perth.

We attracted some very high caliber names, in the lithium space, to look at the project. That process resulted in the joint venture, with Ganfeng. They are actually one of the world's largest lithium companies, the largest lithium chemical producer, with a market capitalization of over $40 billion U.S. They are very active, in the space, at the moment, growing their portfolio of assets on the raw materials side, especially in the downstream. I think they've recognized that putting your foot on the raw material is just as important. We are only a couple of months into this relationship, but I'm very pleased, with the proactive engagement and the encouraging commitment that they have made, along with us, to expedite that definitive feasibility study, update and progress to final investment decision, hopefully earlier this year, ahead of what we then planned to do with the demerger.

Dr. Allen Alper:

That sounds excellent. It's fantastic to have two such outstanding projects. Michael, could you tell us a little bit about your share and capital structure?

Michael Anderson:Firefinch has been around, as an organization, for probably around 10 years. We have had a couple of name changes, the most recent of which was Firefinch which came up with the acquisition of Morila. Prior to that, we were called Mali Lithium, when we were focused on the Goulamina Project solely, and prior to that Birimian Gold, which back in the day had a relationship with Morila, having transacted on the satellite projects that we're currently working on. We’ve been around, and that sees us having a rather large number of shares on issue. We have over 900 million shares on issue.

We have a wide-open register. We raised some money, back in June, and did attract over 20 new institutions to the register, but we are still a largely retail-focused stock, with pretty reasonable levels of liquidity in recent months. Today's share price is around 60 cents, with a market cap just a touch over $550 million AUS. When we do the demerger, in the spinout, it will be an in-specie distribution to Firefinch shareholders. Firefinch, itself, will retain probably around 20%. So, 80% of that new stock will be distributed pro-rata.

The ultimate ratios and metrics will be decided a little closer to the time. Very importantly, we raised $47 million AUS, in June and at the end of the June quarter, we reported over $60 million of net cash and bullion, which sees us well placed to move forward, with our current activities.

Dr. Allen Alper:

That sounds excellent, it sounds like a great position moving forward. Could you tell our readers/ investors the primary reasons they should consider investing in your Company?

Gold Pour at Morila

Michael Anderson:

It's all about value and return on equity. Our share price has rerated nicely, in the last few months, but we're far from done. This is just the beginning for this Company. We're ramping up, Morila, from what we expect to produce 50,000 ounces this year to 120, 170, 200 in subsequent years. When we do that, there's a significant amount of value that will be ascribed to us on the gold side.

On the lithium side, I think the market is really only just starting to take notice of Goulamina. For a long time, housed within Mali Lithium, the project was stalled. The partnership with Ganfeng has completely transformed the opportunity. We now have a very clear path to funding for construction and getting into production by 2023 is the plan. When you look at the peers in that space and Goulamina shapes to produce over 400,000 tons of spodumene concentrate. The companies that are doing that, at the minute are capped at billions of dollars.

On both fronts, we can see a significant value to be realized. That's the opportunity for shareholders getting in. This Company has its foot on two fantastic assets that we believe will deliver significant upside from here, in the coming months and years ahead. Both companies, we're confident, will also have a very open mind about growth through merger and acquisition. This Board and Management Team have done multiple deals before and these two deals; the acquisition of Morila and the joint venture with Ganfeng, are a testimony to a very experienced Team, capable of transacting and adding value.

That sounds outstanding! Sounds like a great opportunity for our readers/investors. Michael, is there anything else you would like to add?

Michael Anderson:

Thank you. I appreciate the opportunity to speak with you and to reach your readers/investors.

Dr. Allen Alper:

Thank you. We’ll publish your press releases as they come out so our readers/investors can follow your progress.

https://firefinchltd.com/

Dr Michael Anderson

Managing Director

Firefinch Limited

info@firefinchlimited.com

+61 8 6149 6100

|

|