Goldgroup Mining Inc. (TSX: GGA, OTC: GGAZF, BMV SIX: GGAN.MX): Canadian-Based Gold Production, Development and Exploration Company with Assets in Mexico and Ecuador; Interview with Keith Piggott, President and CEO

|

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 3/20/2017

Goldgroup Mining Inc. (TSX: GGA, OTC: GGAZF, BMV SIX: GGAN.MX) is a Canadian-based gold production, development and exploration company with assets in Mexico and Ecuador. Goldgroup owns the producing Cerro Prieto gold mine in Sonora State, Mexico, as well as 50% interest in the DynaResource de Mexico S.A. de C.V., which owns 100% of the near-term San José de Gracia project known as Sinaloa State's "Most Significant Gold Project". We learned from Keith Piggott, President and CEO of Goldgroup Mining, that Cerro Prieto is a stable, good cash-flow operation that keeps Goldgroup effectively out of any debt, and they are making modifications to increase gold recovery even further. Recently Goldgroup expanded to Ecuador, where they have a property, which is expected to be a small low-cost run of mine heap-leach gold mine called El Mozo. The Company expects the project to begin production at the end of 2017. According to Mr. Piggott, Goldgroup is looking forward to an extremely exciting future in the very near term.

PDAC 2017: Keith Piggott, President and CEO of the Goldgroup Mining

Dr. Allen Alper: This is Dr. Allen Alper, Editor-in-chief of Metals News, interviewing Keith Piggott, President and CEO of Goldgroup Mining Inc.

Could you give our readers/investors an overview of your company?

Keith Piggott: Nice to be with you Allen. This company has been formed for a number of years. Currently it has one operating mine in northern Mexico. It’s a very successful operating mine, producing around 20,000 ounces this year. Operating costs are expected to be around $900 an ounce in 2017. It's an open cut, heap-leach operation with agglomeration, and it's currently undergoing a small expansion to increase recovery from the current 65% up to what we hope will be 75% by putting in some extra crushing capacity. We've also taken on some extra ground, so we expect, over the next few years, to explore that ground and the near vicinity, and increase the ore resources for the operation. This is a stable operation, with good cash flow. And the company has minimal debt.

We have an exploration property, development property in Ecuador called El Mozo. It's a high sulfurdation, totally oxidized system in Central Ecuador. We've decided to open up into Ecuador because it's a good country to go to now. It has very progressive mining laws and there's some low hanging fruit there. And El Mozo is a small open cut to start with, to get us going. We expect to be in production sometime this year, with a production rate similar to Goldgroup in Sonora, Mexico, around 20,000 ounces a year; however, at a much lower production cost. A production cost of around $600 an ounce instead of $900 an ounce. And the reason for that is the recovery is much higher. It’s a heap leach system similar to Purina and Yanacocha in Peru. It's in the same gold belt, but into Ecuador, north of there. It was drilled by Newmont a number of years ago. They put 57 holes into it so we're very happy the ore is there and it probably has about a 10 year mine life without any expansion.

The capital cost is extremely low because it doesn't need any crushing. It’s a run of mine, heap-leach. Very similar to Yanacocha and Purina in Peru. So that's very exciting for us. Goldgroup also has a property in Sinaloa, which has been in dispute for the last six or seven years with an American company. That dispute is expected to be resolved this year with the help of the Sinaloa government because it's reckoned to be the richest gold deposit in the state of Sinaloa. It has over a million ounces in resources and it's the sort of operation that can be started up very economically. Its average grade is six grams to the ton. It's a very economic deposit to put into production and it will be expected to produce 50,000 or 60,000 ounces of gold in the first year. So that, we believe, will be settled this year. We've already won an arbitration decision in the current year, which we are in the process of enforcing in the US. So we are finally making progress and see a favorable resolution in the near future. So Goldgroup is looking forward to an extremely exciting future in the very near term.

Dr. Allen Alper: Well that sounds great. Could you tell us a little bit about your background, your management and your board?

Keith Piggott: When we had the problems with Goldgroup a few years ago, we had two extremely rich properties, which Goldgroup had developed, which we were forced to sell to Timmins Gold Corp. And now, Timmons has sold it to some friends of mine in a company called Candelaria. We were forced to sell that to keep Goldgroup alive, unfortunately; however, I'm a mining engineer and I basically take properties which have some exploration and explore them further and develop them into mines. I've done it very successfully in Africa, in Australia, in Papua New Guinea, in Mexico, and now in Ecuador. So I'm very experienced. I've done this about 20 times in my life, different mines in various countries, most of the time with extremely good success rates. I'm reckoned to be a very good explorer, but not a grassroots explorer. I normally take things that have been partly explored and develop them, and turn them into mines. And I reckon that's my forte.

My nickname in both Ecuador and Mexico is the magician because people say I can put things together with little capital.

Dr. Allen Alper: Well that's great. Could you tell me a little bit about your share structure?

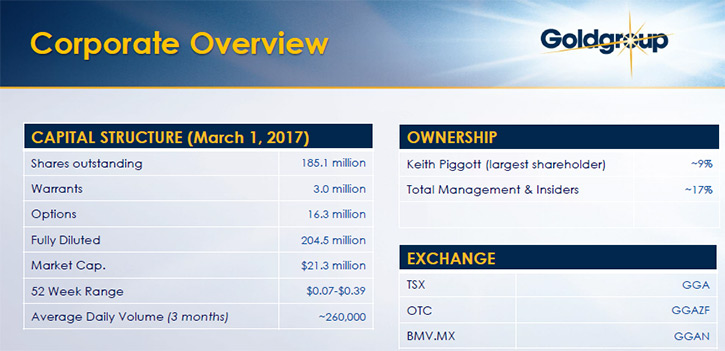

Keith Piggott: Currently, Goldgroup has approximately 185 million shares out. Management and insiders own approximately 20% of the shares. Insiders and friends of the management would probably hold another 20%. So there's probably about 40% of that entire shareholding in float. I personally hold 10% of the company. Goldgroup’s share price is 10 cents a share and it was recently as high as 35 cents a share. There was a letter writer who told his readers to sell and they all sold in block, pushed the share price to around 25 cents, and people then said, "Well, why are people selling?" Well, they sold because they made a profit. They didn't sell because they didn't like the shares. So I'm fortunate to push the share price. I believe firmly that this company currently has a market cap of about $20,000,000. I believe that with the current producing mine, its ore resources, its near imminent production in Ecuador, and it is near term production in Sinaloa. I believe that the company is extremely undervalued in this current market.

So I believe with a slight higher Gold prices, the upside potential of this company, with these current prices is extremely good.

Dr. Allen Alper: Well that sounds very good. What are the primary reasons our high-net-worth readers/investors should consider investing in your company?

Keith Piggott: Yeah. We think the company has a good upside potential for many times the current share price in the short term because of the points I've already made. Because it has a stable producing mine, with increasing cash flow due to the increasing recovery from the expansion we're doing right now, which should be completed by the end of March. So we've spent probably close to $2,000,000 putting in new crushers, new screens, and increasing recovery in throughput. We've recently purchased three 100 ton trucks to give us increased output. So we're running two loaders, three 100 ton trucks, plus the smaller trucks, which will maintain increased throughput through the crushing system. So I think Goldgroup is self-financed. We don't need to go to the market at all anymore. We have enough money for exploration on our expanding concessions. Expanding production gives us that. And we have these operations coming on stream, which will be self-financed in Ecuador because we'll be using contractors to mine.

So there's very little expenditure there. All of our expense will come out of internal cash flow. And in the San Jose de Gracia area, with over a million ounces of gold in the ground, I think it is really, really exciting for us, again, in the near term. So I think high-net-worth readers/investors should consider Goldgroup as being a potential part of their portfolio because of the very high upside potential.

Dr. Allen Alper: Thank you very much. Is there anything else you would like to add?

Keith Piggott: I'd just like to say Allen, thank you very much. I've known Allen for several years now and we've had a few interviews over the years. We've been through fairly significant down-turn in the gold price and in the market, generally. I personally think from 2017 to 2021, in the next four years, we should see a reevaluation of the commodities, especially gold, creeping up, real interest rates staying down because in Mr. Trump's own words, he wants to expand America within America. The only way he can do that is to have a relatively weak dollar and low interest rates. There's no way that he's going to explore with a high dollar and move his economy forward, with high interest rates. So I believe that is Mr. Trump's own view of America and basically for the rest of the world. Everybody wants their currency to be lower than somebody else's.

And what does that mean? It means a high price for gold. So I think we're in for a really good round for the next few years. Albeit this summer, we might go into the summer and not see a high price for a few months, but I believe coming in August, September this year, we're set for a really good gold market. And that's really good for small mining companies with good potential.

Dr. Allen Alper: Well, thank you very much.

Keith Piggott: Allen, thank you very much. Very kind of you.

https://www.goldgroupmining.com/

Suite 1502, 1166 Alberni Street

Vancouver, BC

V6E 3Z3 Canada

Tel: 1.604.682.1943

Fax: 1.604.682.5596

Toll Free: 1.877.655.ozAu (6928)

Investor Relations

Email: info@goldgroupmining.com

Tel: 1.778.330.2759

Toll Free: 1.877.655.6928

|

|