Interview with Ian Stalker, CEO K92 Mining: Vancouver based gold producer with operations in Papua New Guinea

|

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 3/2/2017

K92 Mining is a Vancouver based gold producer with operations in Papua New Guinea. The company has commenced gold production from the Irumafimpa Gold Deposit at their Kainantu Gold Project that was previously mined by Highlands Pacific and Barrick Gold and has existing infrastructure, including underground mine development, mill processing facility, staff housing, licensed tailings pond, office space, paved access roads and reliable hydro supply via a dedicated power line. We learned from Ian Stalker, who is CEO and director of K92 Mining, that by the end of the first quarter 2017 they will be cash flow positive and by the middle of 2018 they plan to turn from junior to a mid-cap company.

Dr. Allen Alper: This is Dr. Allen Alper, Editor-in-chief of Metals News, interviewing Ian Stalker, who is CEO and director of K92 Mining. Could you tell us what differentiates your mining company from other mining companies, and about your property or properties in New Guinea?

Mr. Ian Stalker: Sure, Allen. Thanks for the invitation. Let me address the first point. To differentiate ourselves from the bulk of the other juniors out there in the marketplace consider the following : first we are currently under production startup mode, building up to a steady-state operation, which we believe will occur by the end of the first quarter 2017, so over the next two months. At the end of that period, obviously we're in a cash flow positive situation, which is an excellent position for us. Unlike our competitors we're not having to go to the market for excess cash, etc. so that's a bonus.

Over and above that we have the base case, which is our Irumafimpa mine. That's the one that is under startup. BUT we also have a well-developed project called KORA, which is an ore body along strike from Irumafimpa, only 700 meters farther away from where the existing adit access stope drive goes under the mountain. We'll be commencing that drive to get over to KORA early in 2017. We think we'll be starting work in January, so literally tomorrow. When we get over there, we think we can mine KORA at twice the rate we have at Irumafimpa i.e. 110k ozs Au equivalent per year.

We have a nice base case, decent cash flow kicking in really now and building to a steady state by end of first quarter. By the middle of 2018, we expect KORA to deliver into our production scenario. That means we can double our production rates, and so our little junior almost blossoms into a mid-cap type company. Throughout this period from now until early 2018,, as we start to get that information out and people start to see the progress we're making over in Irumafimpa and KORA, people will see the value being unlocked, and the investment potential that really exists. If gold goes up as we expect, our value should be even higher, so that differentiates us significantly.

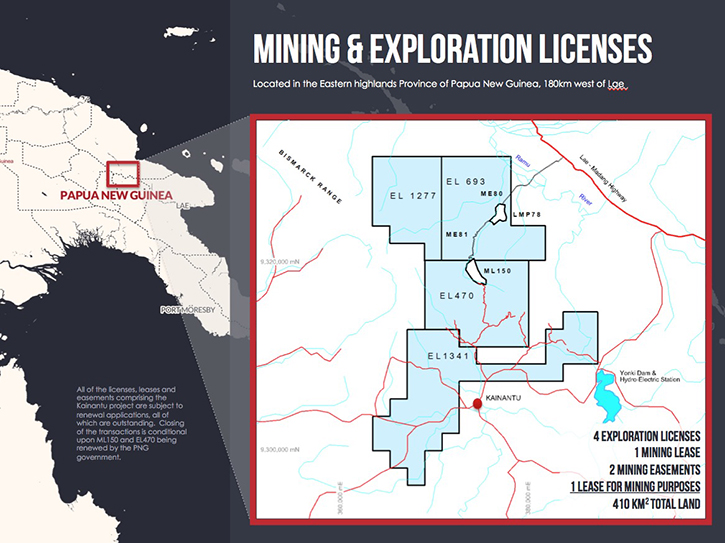

We bought this project from the world's number one gold mining company Barrick in 2015, finally got funding at the beginning of 2016 and started rehabilitation work on what was an existing mine and an existing infrastructure. Barrick bought this entire project and the package which is 400 square kilometers of ground back in 2007 because they felt there was a very good opportunity to develop and deliver into the greater Barrick total resource numbers, a mine resource, similar in size to others in Papua New Guinea that is greater than the current 2million ozs we have under 43-101 today. Papua New Guinea is not known for small mines, they're actually well known for large mines as in Pogerra.

We picked the project up very cheaply because of the systems, guarantees, the timing in the marketplace, etc. and it fits our business model well. We then battled in a tough market to get it funded, but we did so and we're moving forward positively. But, the extra opportunity, outside of what I've just described in terms of restart and then moving into the intermediate stage, is the bigger picture, the exploration potential, near-term, medium-term, and long-term is a terrific opportunity.

We are delighted to be owners of this mine. It's in Papua New Guinea, a remarkable country in my opinion. It does have its challenges. But in comparison to other countries, the Govts. mining regulatory authority, called MRA, has the most efficient bunch of guys and they are very supportive. They make a tough job just that little bit easier.

To give your readers a bit of an idea of the quality and drive of the people of Papua New Guinea. Recently they just finished the under 20 ladies' World Cup Soccer tournament, which was broadcast from Port Moresby to somewhere around a hundred and eighty million viewers worldwide. When you think of that kind of event in a country like Papua New Guinea, you start to realize that perhaps it's a lot more stable and moving positively into the kind of environment investors like to invest in. Add that criteria to the fact that we have such a great project, and I think in this case one and one doesn't just make two, it makes twenty.

Dr. Allen Alper: Sounds great. Sounds like you have an excellent property and great potential, and you have the opportunity to generate cash flow in a very short time compared to most mining companies. I noticed you have a very strong team and you have a great background. Could you tell our readers about yourself, your team and your board?

Mr. Ian Stalker: Sure. Delighted to. If anyone has seen my picture, they will see an older grey-haired fellow, and the reason behind that is I've been in the mining industry over 40 years now. I've been lucky enough to be involved in a range of project construction, project development, and mining operations from start, i.e. resource evaluation into project development and finally into steady state operations. I've been lucky enough to be involved in ten of them worldwide, with companies such as Goldfields of South Africa. Probably the one that really got my foot in the ground was a company called Ashanti Goldfields, which was the real premier company within Africa during the 90s. 1990-1998. I think that’s quite an achievement and I'm delighted to be able to tell you that, Allen. That was good experience in terms of opening operations, gold mining development, and then I was lucky enough to be involved in the junior space with quite a few junior companies who returned some great investments for people who come in at the right time.

One of them was, of course, the company UraMin, Inc. that was sold for $2.5 billion in 2007 from a relatively small market cap in 2006. The second one was also a uranium play that did very well for the investors in London, then recently, of course, we were lucky enough to get Brazilian gold, which was a company, based in Brazil. But I'm only one part of the entire setup. Tookie Angus is the chairman of the board. He is a well-experienced mining entrepreneur, with a legal background and solid M &A type experience. He has an exceptionally good grasp of mining operational demands and the cut and thrust of the mining operations business, which is what we are. He's currently Chairman of Nevsun. He too has a great pedigree.

Bryan Slusarchuk, our president, is more a capital markets type individual, more a marketing person, but also has run and has been CEO of companies, good guy to have on board. He really works with me in getting our message out.

We have a well spread board with a range of skills that complement each other. That’s important because it is a challenge as a small company to do the same stuff that a big company does. The right team just makes life easier.

John Lewins is the Chief Operating Officer, very important to us. He has 30 plus years in the mining business. He worked internationally in a range of companies in gold in particular. He has been in Papua New Guinea, and that knowledge of Papua New Guinea was one of the reasons John came on board. He put together a team of people on site, about 15 ex-patriots now, making sure that we have adequate cover for the shift operations, and for the range of disciplines that you need to run the mine. They all have a background in Papua New Guinea. They were not going over there with their eyes closed. They all know how to work in Papua New Guinea and that allowed them to settle in just a little bit quicker.

John's done a terrific job in putting this together. One of the things I recognized early on was that running the company from Vancouver, with the mining operation being over in Papua New Guinea, that there is a fair old distance between the two. John lives over in Australia and has two flights to take to get into PNG, one to Brisbane and another into Port Moresby. It's a lot easier, he's in the same time zone, so when things happen as they invariably do in an operation, he can resolve the issue in a timely manner, and he needs both experience and the backup team to do that. In any remote mine, and most of them are these days, the quality of the people on the ground makes a heck of a difference A poor team can turn a good project into a bad project, but a good team can make a difficult project into a well-run project and I think we have a great team.

Dr. Allen Alper: It sounds like you have a great team and you have the background to move it forward in production. That's excellent. It's a very well balanced team, which is great. Can you tell me a bit more about your resources?

Mr. Ian Stalker: Sure. We have, plus or minus, 2 million ounces in the 43-101 compliant resource statement, of which the initial material coming out from Irumafimpa is predominantly indicated a little bit in the measured category, and that has a mine life, at the current mining rate as we understand it, of eight years. At the moment, we've only detailed a month by month typical operation budget over 30 months coming from Irumafimpa, because the bulk of our resources sits over at KORA, and we believe KORA is a more economic prospect. It's that ‘along strike resource’ that I mentioned, which contains roughly about 1.6 million ounces or thereabouts. We believe by mining at 400,000 tons a year, which is what we know the process plant is capable of doing, with a few minor modifications, and by spending only approximately $14 million of Capital, we can double the rate we are achieving currently from Irumafimpa from KORA and we can have a 10 year life of mine, producing about 110,000 ounces( Au equivalent) a year, so the existing resources gives us a super project without having to find another ounce and a great investment return on the expected $14m of Capital.

Over there, the site of the operation is in the valley, and the mine itself is up in the hills. Although we call it an underground mine, it's actually an elevated mining operation. We drive into the hill site to access it. In the realities of discovery, all the drilling was done from the surface and because it's quite tough topography, it's challenging and costly to get the drills up there as well as all the infrastructure that's needed to get the drilling done, and so only a limited amount of drilling was done in the early days Also, you've got to get things like local agreement on getting access and permits and so on and so forth.

The lucky thing for us going forward, Allen, is that as we drive over from Irumafimpa to KORA, we will be drilling from underground. We believe that these two resources will actually combine quite nicely. We think this new drilling info will give a huge boost to the overall resources that we are currently reporting, and the nice thing is that we're doing it from an underground scenario, so it's cheaper. You don't have to use helicopters and pads, etc. It's quicker because you're not drilling through the surface to get to the ore body down below you, you're actually in it, and of course, it's less intrusive in having to deal with local communities, because the underground is under your own control within the mining lease. Everything for the increased tonnage is fully permitted already

I think for our little company, our resource is going to grow. We're optimistic in terms of its size. We think it can be two, three times where we are at the moment, maybe even three, four times. That's according to geologists, with pretty good credentials such as Doug Kirwin. We've asked Doug to look at our resource numbers and our exploration potential. If we're right, phase three for little K92 is not the 110,000 ounces, it's exactly what we do with a much bigger resource and how quickly you mine it. It's hugely exciting.

Dr. Allen Alper: That sounds excellent. Could you tell me a bit about the cost of operation?

Mr. Ian Stalker: The total capital up front is about $14 million for putting in phase two, the KORA development etc. There is a sustaining capital for internal development, raises, etc. over the 10 year life of a mine of about $62 million, but it generates as a consequence of a very good free cash flow, using $1250 as a gold price, that makes it a no-brainer in terms of we're going to do it. We just completed our internal budget. When we settled down to steady state at Irumafimpa, the startup mine, the cash costs will be sub $600/oz, and the all in sustaining costs for that period of time we're running Irumafimpa will be roundabout $660/oz.

When we get to KORA, of course, with the higher productivities, the greater width of the ore body and the greater mining rate, remember I said it was twice what we're going to be mining out of Irumafimpa, then those cash costs come down another little bit and the sustaining costs gets close to the $620/oz. Very competitive cost profile numbers anywhere in the marketplace, which gives us a level of comfort that despite the pain that we're all feeling, and it's painful, we're quite sustainable going forward.

Dr. Allen Alper: That's excellent. That's very good. Very competitive. Could you tell me a bit about your share and capital structure and where you're listed, etc.?

Mr. Ian Stalker: We're listed on the TSX and our trading symbol is KNT, and our name is K92, so the N is for 9, and the T is for 2, so KNT is our trading symbol. We have an approximately 120 million shares out there at the moment, and fully diluted we would go up to about 150. The interesting thing in the fully diluted number, Allen, is that the bulk of them are warrants, a lot of them still at 50 cents, $1.50 or $1.75, so if everyone were to vest their warrants, then of course it would bring another 15 to 20 million dollars into the treasury, which would be well received of course. Approx 50 percent of our stock is held by institutional type owners, about 25 to 30 percent in retail, and about 20, maybe 25 % with insiders/management so nice, tight share owners, and not the excessive number of shares you see in a lot of companies.

Dr. Allen Alper: That sounds very good. What are the primary reasons our high-net-worth readers/investors should consider investing in your company?

Mr. Ian Stalker: Well, I think the growth potential is huge. One of the challenges in any commodity related marketplace that you face is one, raising the capital, and then two, using the capital effectively. In our case, the capital risk is taken away. The mine's already in place, the process plant is there, and $14 million of Capital to get us to the 110Au oz p.a. production level is by comparison to the kind of cheques people need to sign for a new operation relatively low. All the permits are in place. We have permits for a 10 years mining license, we have environmental permit for 25 years, we have the access permit, permit from the road, and I should tell you we're very close to the main paved highway from Lae, the second largest city. We're in the process of completing, and in fact have completed the power contract, which means that, unlike a lot of our competitors in the mining business who are remote, and have to rely on diesel for their power generation, our power generation comes from a hydro power source, which is then delivered into site by about 40 k's of cabling, etc. It's already in. We've signing a contract for that operation to continue and some upgrading that's going to be managed by the power supply company themselves.

There is a risk too of being caught in the pendulum movement of oil prices going up, this means that a lot of costs for a lot of big mining companies that are an open pit scenario are well as underground however with our Hydropower supply to our site we don't have this risk. I think our operating costs are going to be pretty stable too going forward. Of course we expect to see this resource grow and grow very quickly, and so depending how you want to value the company both in terms of cash flow or in terms of resource numbers, I think there's quite a significant bit of upside in both. Being in Papua New Guinea, being a TSX listed company, is not a bad place to be.

Bear in mind the big companies in Papua New Guinea. Newcrest is the largest independent one out of Australia , Lihir is there, Freeport McMoRan is there, Harmony, one of the largest gold mining companies is there and of course Barrick themselves, the number one gold mining company, remains there in that 50 percent joint venture up in Pogerra. It's not such a bad place to be investing.

Dr. Allen Alper: Sounds like excellent reasons why our readers and investors should consider investing in your company. Is there anything else you'd like to add, Ian?

Mr. Ian Stalker: I'd love to tell you that I thought the gold price was going to change today, back up to $1250. It would be fantastic. I do think we'll get back there within a period of time.

http://www.k92mining.com/

Suite 488 – 1090 West Georgia Street

Vancouver, British Columbia

Canada V6E 3V7

Mario Vetro

Office: +1-604-687-7130 x200

Cell: +1-778-846-9970

Email: ?mvetro@k92mining.com

|

|