Interview with Michael Philpot, Executive Vice President: Coro Mining (TSX: COP): Growing Chilean Producer of Copper Cathodes and Copper Miner

|

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 7/8/2016

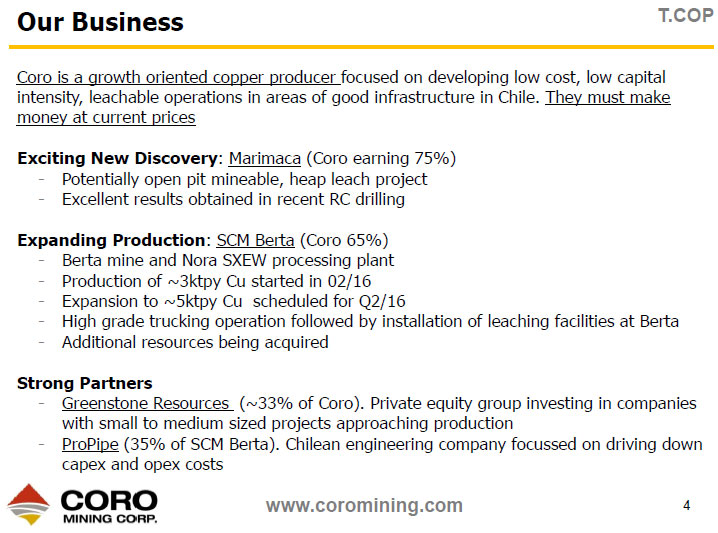

Coro Mining Corp. (TSX: COP) is a growing Chilean copper producer that started producing copper

cathodes from their Nora Plant located in the 3rd region of Chile, near the Berta copper deposit

discovered and developed by Coro. The company linked the Berta mine to the Nora Plant and started

production at 3000 tons per annum, which is about 6.5 million pounds of copper, and they are in the

process of upgrading to 5000 tons (or 11 million pounds) of copper cathode. Recently Coro made an

exciting copper discovery at their Marimaca project located in the 2nd region. According to Michael

Philpot, Executive Vice President and Director of Coro Mining, the company is blessed with a great team

and very good partners, including very strategic working relationships with Greenstone Resources and

Pro-Pipe. and they have been running a successful business enterprise even during the low point of the

copper cycle. Coro is growing by exploring and finding to financing, developing and producing copper in

coastal Chile. They have made very strategic working relationships with Greenstone Resources and Pro-

Pipe.

Mobile Crusher

Dr. Alper: This is Dr. Allen Alper, Editor-in-chief of Metals News interviewing Mr. Michael

Philpot, who is Executive Vice President and Director of Coro Mining Corp. I know a lot of exciting

things are happening for you right now. You intersected substantial copper mineralization, and you're

also producing in Chile. Could you tell me a little about your company and what's happening in Chile?

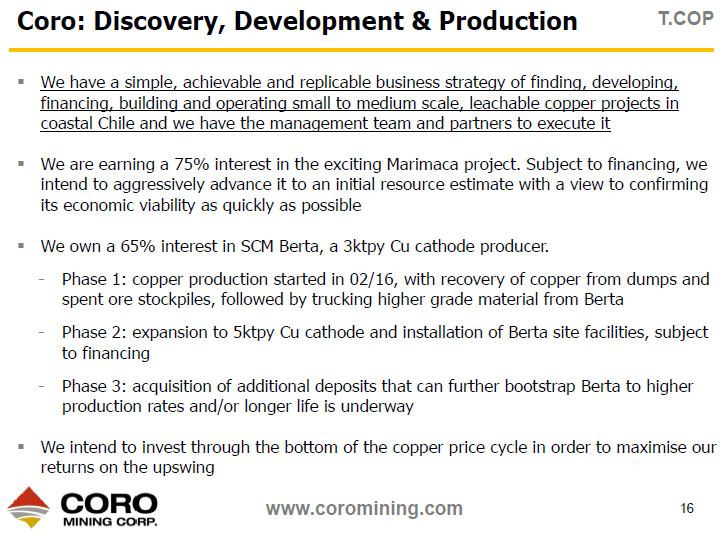

Mr. Philpot: First and foremost, yes, Coro Mining Corp. is a small copper producer. We started

producing copper cathodes from our Nora Plant, which we brought out of administration. The Nora Plant's

located in the third region of Chile, and it's very close to a copper deposit that we discovered and grew

and developed, called the Berta. We linked the Berta mine to the Nora SXEW Plant, and we started

production at 3,000 tonnes per annum, which is say 6.5 million pounds of copper. We're currently in the

process of upgrading that to 5,000 tonnes of copper cathode, which equates to around 11 million pounds of

copper cathode. We do this as a business, nothing more than a margin business. We're quite happy to be

getting a relatively healthy margin even at these copper prices in the 2 to the 2.25 range. This is our

base for building the company.

Around the Nora Plant, we're quite busy on an acquisition front that can, very much like the

Berta deposit that we own, augment further production in the area around the plant. That's either

extending the life of the plant, or looking for an increase in production, at the Nora Plant, maybe up to

something like 10,000 tonnes. This is the growth story of copper and copper cathode production, but

that's just not the only part of the story for Coro Mining Corp.

Coro Mining Corp. is aggressively looking in other areas in Chile and more importantly, quite recently,

up in the second region. Up near the mining city of Antofagasta, we have a fairly good discovery in the

project that we call Marimaca. It did have some little old copper workings on it, so the people who did

the little workings were probably the first discoverers, but it's never had a drill hole on it.

We put in 16 holes over a strike length of about 700 meters on one of these zones (west zone),

and over a strike length of about 300 meters in another zone (East Zone). Every hole came back with

significant intercepts of 100-meter plus, good-grade copper oxide. Good grade, for us, is 0.5 plus. In

this case, ours probably average closer to 0.65% copper oxide. I think we're going to have really good

solubilities, which will provide us with good recoveries, as well. When you hit 16 holes per 16 holes -

I've been in the business for 40, years, and that's a very, very good success ratio. The good thing is

it's very consistent. It's not like one hole with one type of grade, and another hole with a lot grade.

Dr. Alper: Very exciting! Could you tell me a bit about yourself and the team?

AC Tertiary Crusher

Dr. Alper: You're getting excellent results.

Mr. Philpot: We're excited about it. What I should emphasize is that we've barely touched the

surface of what we've found so far. Everything so far has been in the oxide materials, oxide zone, and

also, getting into a mix zone, but I'm absolutely convinced we will get into the hypogene, and that's

more of your sulfide zone down below. There are quite a number of other targets that we've identified by

just geochemistry, geology, also on the property, as well. Yeah, I think Marimaca is the start of a very

exciting project for us, and, most importantly, it shows the ongoing growth in our business, being

copper, in the stable country of Chile moving forward. Exciting times!

Mr. Philpot: We have a great team of people. Our company is mostly very high-level Chilean

engineers and geologists. Our head of country management is Marcelo Cortes, who worked for Antofagasta

Minerals. He looks after most of our activities down in Chile. He's augmented by our VP of exploration,

Sergio Rivera, who is the ex-Vice President of exploration for Codelco, the largest copper-mining company

in the world. My partner is Alan Stephens. Alan lives over in the UK, but travels extensively down to

Chile. Alan was the VP of exploration for First Quantum Minerals, where I met him. Before that, Alan's

had a long tenure with Cyprus Amax. I was one of the founders of First Quantum. So all our backgrounds

tend to be much more focused on copper than other commodities. To have that type of team working with you

is a blessing.

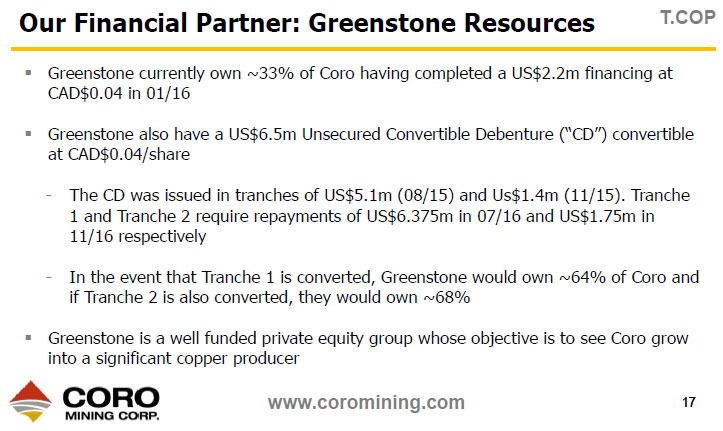

We also have a few very good partners within the company. We have a private equity fund called

Greenstone Resources, which is a London-based private equity group. At the project level, we have a

superb team, a boutique engineering firm called Pro-Pipe. We met them when they were doing a lot of the

work on Berta. During this downturn in the resource business, financing's been very, very difficult.

Pro-Pipe stepped up to the plate and said, "Hey, we really like this project so much that we want to earn

a project stake in the Berta-Nora," and so they did. We have a mix of partners with us to augment the

management team, so we're very fortunate.

Dr. Alper: That sounds very good. Sounds like you're well-positioned. You have an

experienced group there. Not only management, but also with local engineers in Chile, and you're getting

support from an engineering group. That sounds great.

Could you tell me a bit about your capital structure and your finances?

Mr. Philpot: Currently we have 380M shares outstanding with Greenstone holding 58%, Management

7% and institutions 4%. The Company has no debt. We are currently completing Tranche 2 of a C$10M private

placement which will likely see a slight shift in core participants shareholdings slightly.

When Coro Mining Corp., through Greenstone, bought the plant out of administration, Greenstone

was good enough to provide a convertible debenture to Coro Mining to at least pursue the acquisition, so

there is a convertible debenture out on Coro, which, at our choice, we can repay at approximately 6.3

million dollars US, or Greenstone has the unity to convert shares at 4 cents. Upon Closing, the above

Private placement funds will be used to advance the Marimaca project to a resource status, complete

metallurgical work and an early stage 43-101 engineering study.

Dr. Alper: Looks like, in the last month or so, the market may have recognition what's been

going on at Coro Mining Corp. Your stock price has dramatically improved. Sounds like things are getting

ready to improve more, and it might be an opportune time at some point to raise funds.

Mr. Philpot: I truly think so. I think, with everything within the company today that we see

and envision, it would not be a stretch to see Coro Mining producing at 30,000 tonnes of copper capital

per year for the next 5 years. So that is our objective. We don't need to go out and look for anything

other than what we already have within the stable of the company.

Dr. Alper: That sound very, very good. Could you tell me, what would be the primary reasons

high-net-worth readers, investors should invest in your company?

Mr. Philpot: I think, first and foremost, they have to like the commodity of copper. Coro is

copper, and then being in a very stable jurisdiction like Chile provides a lot of support, and Chile is

also the # 1 copper producing country in the world. Management is very important. They have to believe

that management has the capability to exercise or fulfill their business strategy and business plans.

Coro Mining Corp. is not just one project. We expect it to do much, much more than produce a

small amount of copper for the next five or ten years. It's very, very much about growth, and when we

look at growth in these markets, we want to do it through our cash flow, and also working with our Pro-

Pipe partners, doing it in a very austere manner. We're keeping capital costs right down to the bare

minimum. We're being very creative in a lot of our ways of providing that growth. We're running a

successful business enterprise in the low point of the cycle of copper. If you believe the copper price

does have a brighter future, and may return to the 3 dollars and 4 dollars of the past, then there's a

phenomenal leverage to the price of copper. Plus the great lift from the development of the projects and

the stability of the growth moving forward.

Dr. Alper: Excellent. That's very, very good.

http://www.coromining.com/

Suite 1280 - 625 Howe Street

Vancouver, BC

Canada V6C 2T6

Tel: +1 604 682 5546

Fax: +1 604 682 5542

Info: investor.info@coromining.com

Corporate Presentation: http://www.coromining.com/i/pdf/COP_CP.pdf

|

|