A Monday Morning Musing from Mickey the Mercenary Geologist

Contact@MercenaryGeologist.com

November 14, 2014

A multitude of mavens,

pundits, sages, wizards, writers, and assorted talking heads with various but vested

interests in the hard commodities sector have weighed-in on the supposed demise

of the secular bull market in “stuff” over the past few months.

Reactions have been varied

but predictable: the usual suspects in the gold- and silver-bug camps have

played the market manipulation card to explain the overall weakness in precious

metals prices; the China perma-bears have claimed the downtick in industrial commodities to be a foreshadowing of the

pending collapse of that country’s decade-long economic growth; and the

hyper-inflationists have determined the cause to be big banks that will not

loan their growing stashes of Federal funny money, thus leading to decreased

demand for industrial metals and energy. Meanwhile, the deflationists have

stated we are simply living in a deflationary economic environment. Many have

commented on US dollar strength as a contributing factor to lower commodity

prices.

I say nonsense to most of the

above. In the words and charts that follow, I will provide irrefutable evidence

that the weakness in hard commodities over the past four months can be overwhelmingly

attributed to the strength of the US

dollar. My argument is based on elementary statistics, a general math

requirement to earn a college degree.

As an aside, I had14 hours of

high-level mathematics beginning with engineering calculus in college, but did

not take statistics, a low-level course that would not credit toward my undergraduate

degree. However, it was a requirement when I entered graduate school at the

University of New Mexico. To get around taking a freshman-level math class, I

convinced the geology department that a course shown as “Statics and Dyn” on my

undergrad transcript, was a sophomore statistics course. In actuality, it had

nothing to do with statistics but was a civil engineering course called “Statics

and Dynamics”. LOL.

Let’s

start by reviewing a key concept in statistical analysis: the correlation

coefficient. I’m sure this is way more than most of you need or want to know

but realize I’m a scientist who strives to help lay people understand the

concepts and evidence that support my opinions.

Correlation can be defined as the systematic relationship between

two variables. The correlation

coefficient is an equation that exactly quantifies the linear relationship

between data sets.

A perfect

positive correlation coefficient (+1) means that when one variable increases

the other also increases in an exact relationship; these data will plot as a

straight upward-trending line on an x-y graph. A perfect negative or inverse

correlation coefficient (-1) means that as one variable increases the other

decreases in an exact relationship; data will plot as a straight downward-trending

line on an x-y graph. Complete randomness between two variables, a non-linear

correlation, or other confounding variables all result in a 0 value and the

data will be scattered across an x-y graph.

The

really important thing to note here is the correlation coefficient is a number that

ranges from +1 to -1.

However,

rarely in the real world of measurements, values, prices, or whatever will the

relationship be absolutely perfect between

two variables.

As

you know, I like rules of thumb and they certainly apply here. The following parameters

are used by statisticians to categorize the correlation between two variables:

·

Correlation coefficients

between 0.9 and 1.0 indicate variables that are very highly correlated.

·

Correlation coefficients

between 0.7 and 0.9 indicate variables that are highly correlated.

·

Correlation coefficients

between 0.5 and 0.7 indicate variables that are moderately correlated.

·

Correlation coefficients

between 0.3 and 0.5 indicate variables that have low correlation.

·

Correlation coefficients

less than 0.3 have little if any linear correlation.

Whew!

Now

that we’re finally done with freshman statistics class, let’s look at four-month

charts for the US Dollar Index (DXY) and the three major hard commodities

(gold, copper, and oil) that are listed on integrated world exchanges. That

means they are traded in US dollars via both physical (spot) and paper (futures,

options, warrants, and ETF) markets.

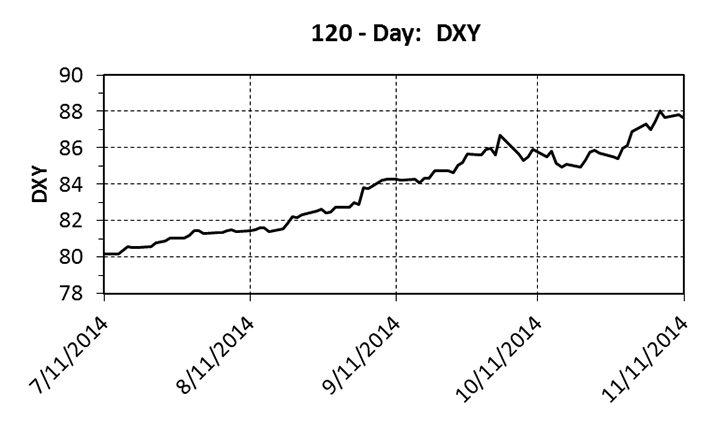

A quick perusal of the first chart illustrates the recent

strength of the US dollar with respect to a basket of world currencies (British

pound, Canadian dollar, Euro, Japanese yen, Swedish krona, and Swiss franc).

Four months ago, the US dollar index (DXY) was commencing its upward march; it

has gone from 80.19 on July 11 to 87.60 on November 11 for a gain of over 9%:

Meanwhile,

prices for the world’s most important precious metal (Au), its major industrial

metal (Cu), and its North American energy benchmark (WTI) have all weakened significantly.

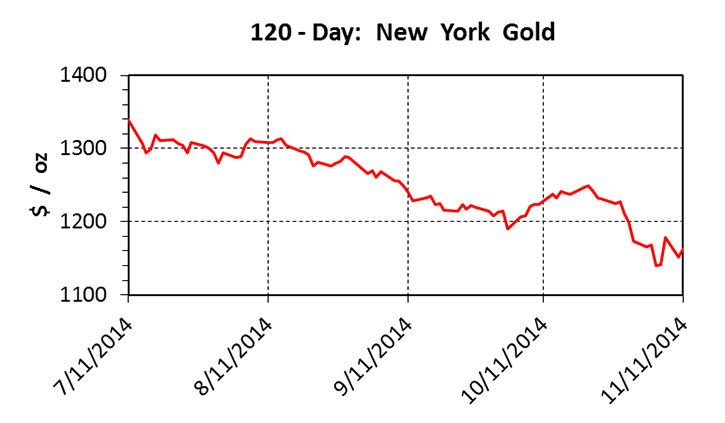

From

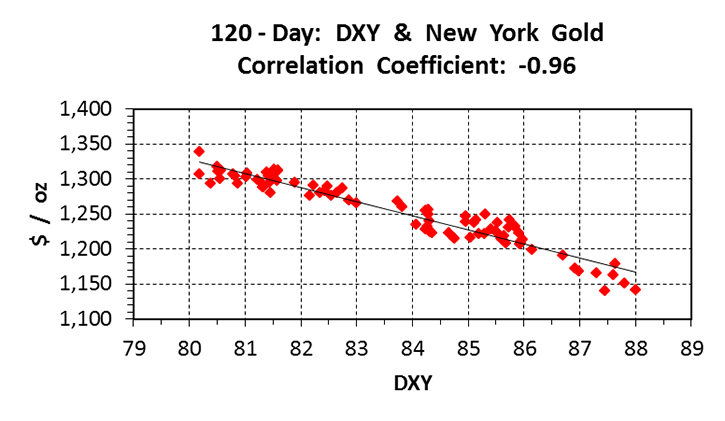

July 11, when New York gold closed at its highest price since mid-March at $1339 an ounce, it has fallen to $1163.

That’s a loss of 13%:

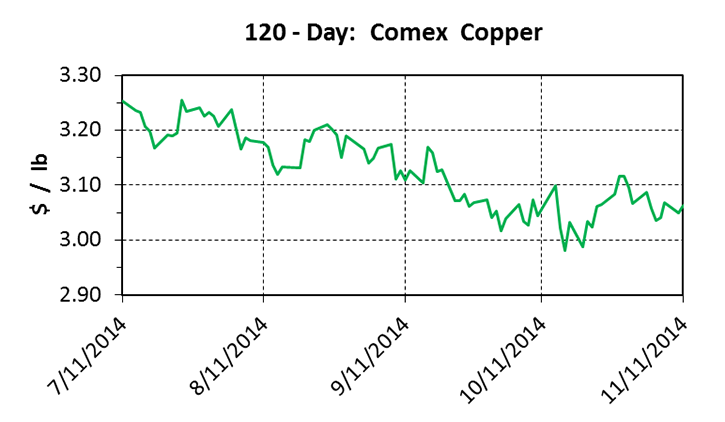

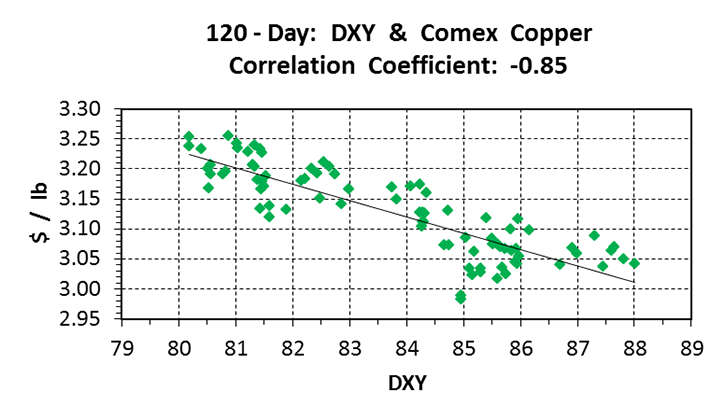

During this same period of time, Comex spot copper

went from $3.24 to $3.06 per pound, a drop of 6%:

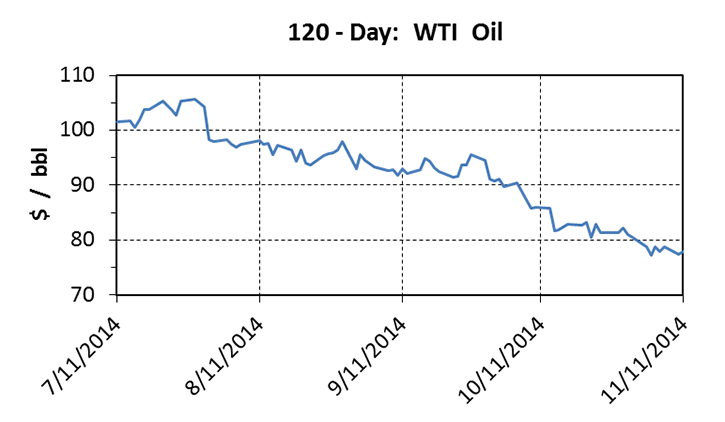

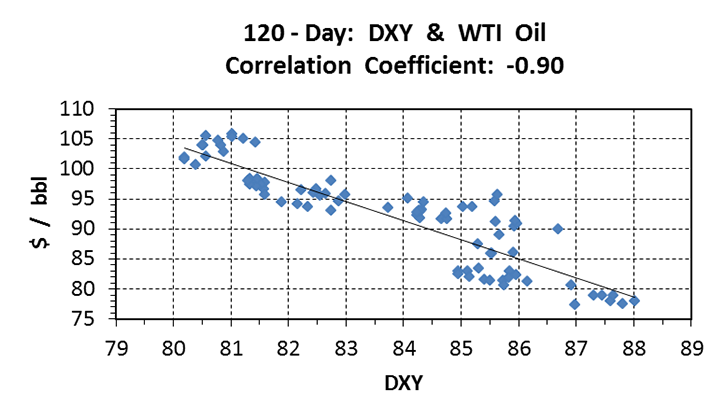

Concomitantly, the West Texas Intermediate crude

oil price has collapsed from nearly $106 to just under $78 a barrel, off a

whopping 26%:

My contention

that the 4-month weakness in commodity prices is directly due to the strong dollar

is shown by the following correlation coefficients and charts. I think they are

self-explanatory:

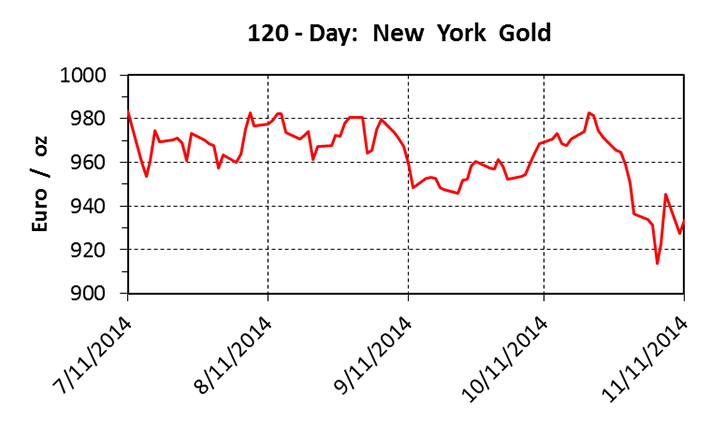

Further evidence supporting my premise is a 4-month

chart showing the price of gold in Euros. Note the relatively minor 5% drop from

€ 984 to € 933, compared to the aforementioned 13% loss in US dollars:

The

four-month commodity and dollar data produce

very high to high correlation coefficients at

-0.96

for gold, -0.85 for copper, and -0.90 for oil.

Although

spot commodity prices are based on short-term supply and demand fundamentals, many

other factors affect their daily fluctuations. Included are industry news,

world events, geopolitics, weather, and natural disasters. Additionally, a good

deal of gaming, arbitrage, and attempts at manipulation are thrown into the mix

with traders and speculators trying to generate short-term profits via the

paper and derivative markets.

Considering

these often competing factors, I view the high negative correlation

coefficients of the dollar index and major hard commodities over the past four

months as quite remarkable.

My

basic statistical analysis has shown the recent drops in major world commodity

prices are simply due to the strength of the world’s reserve currency, the

almighty US dollar. This much-maligned

fiat currency has suddenly and once again become the world’s go-to safe haven.

It

is my contention that given the current world economic paradigm, which includes

a slowdown of growth in China, continuing struggles in other emerging market

countries, European banking and currency woes, and an incipient recovery in

America, the US dollar will continue to rise with respect to other major currencies.

And

a higher DXY implies further deterioration in the US dollar price of all hard

commodities traded on the world stage.

Ciao

for now,

Mickey Fulp

Mercenary Geologist

The Mercenary Geologist Michael

S. “Mickey” Fulp is a Certified

Professional Geologist with a B.Sc. Earth Sciences with honor from the

University of Tulsa, and M.Sc. Geology from the University of New Mexico.

Mickey has 35 years experience as an exploration geologist and analyst

searching for economic deposits of base and precious metals, industrial

minerals, uranium, coal, oil and gas, and water in North and South America,

Europe, and Asia.

Mickey worked for junior explorers, major

mining companies, private companies, and investors as a consulting economic

geologist for over 20 years, specializing in geological mapping, property

evaluation, and business development. In

addition to Mickey’s professional credentials and experience, he is

high-altitude proficient, and is bilingual in English and Spanish. From 2003 to

2006, he made four outcrop ore discoveries in Peru, Nevada, Chile, and British

Columbia.

Mickey is well-known and highly respected throughout

the mining and exploration community due to his ongoing work as an analyst, writer,

and speaker.

Contact: Contact@MercenaryGeologist.com

Disclaimer

and Notice: I am not a

certified financial analyst, broker, or professional qualified to offer

investment advice. Nothing in any report, commentary, this website, interview,

and other content constitutes or can be construed as investment advice or an

offer or solicitation or advice to buy or sell stock or any asset or

investment. All of my presentations should be considered an opinion and my

opinions may be based upon information obtained from research of public

documents and content available on the company’s website, regulatory filings,

various stock exchange websites, and stock information services, through

discussions with company representatives, agents, other professionals and

investors, and field visits. My opinions are based upon information believed to

be accurate and reliable, but my opinions are not guaranteed or implied to be

so. The opinions presented may not be complete or correct; all information is

provided without any legal responsibility or obligation to provide future

updates. I accept no responsibility and no liability, whatsoever, for any

direct, indirect, special, punitive, or consequential damages or loss arising

from the use of my opinions or information. The information contained in a

report, commentary, this website, interview, and other content is subject to

change without notice, may become outdated, and may not be updated. A report,

commentary, this website, interview, and other content reflect my personal

opinions and views and nothing more. All content of this website is subject to

international copyright protection and no part or portion of this website,

report, commentary, interview, and other content may be altered, reproduced,

copied, emailed, faxed, or distributed in any form without the express written

consent of Michael S. (Mickey) Fulp, MercenaryGeologist.com LLC.

Copyright © 2014 Mercenary Geologist.com, LLC. All Rights Reserved.