Elemental Royalties Corp. (TSX-V: ELE, OTCQX: ELEMF}: Gold-Focused Royalty Company, Lower Risk Precious Metals Exposure, Portfolio of Nine High-Quality Royalties; Frederick Bell, CEO Interviewed

|

By Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

on 5/31/2021

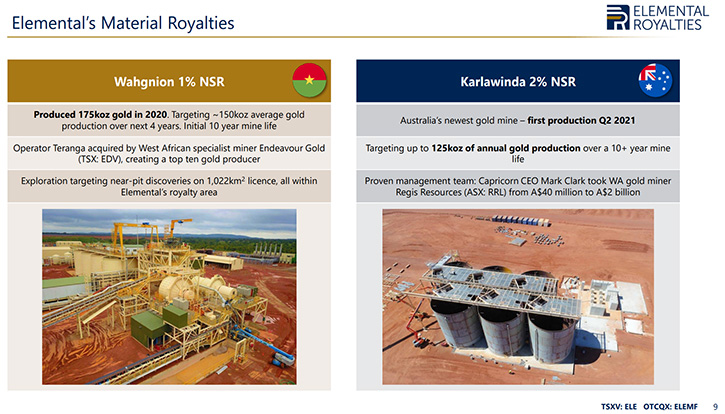

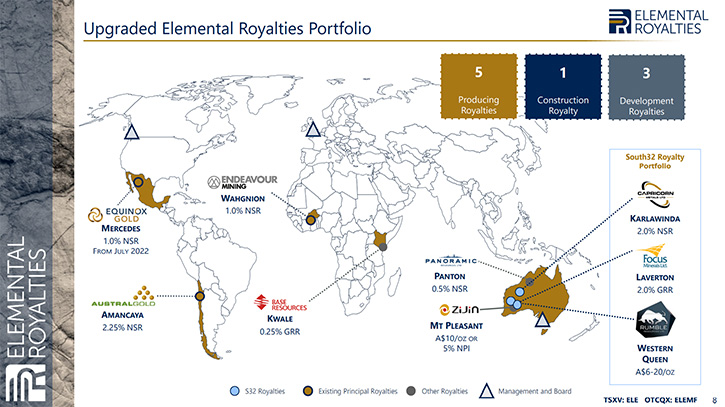

We spoke with Frederick Bell, CEO and Director of Elemental Royalties Corp. (TSX-V: ELE, OTCQX: ELEMF), a gold-focused royalty company that provides investors with lower risk precious metals exposure, through a portfolio of nine high-quality royalties. The Company's approach is to secure royalties, over advanced assets, with established operators from a robust geographically diverse pipeline. This enables investors to benefit from ongoing royalty revenue, future exploration upside and low operating costs. We learned from Mr. Bell that the current biggest revenue earner and a cornerstone asset is a 1% NSR royalty on the Wahgnion project, owned by Endeavor Mining, targeting ~150koz average gold production over the next 4 years, with initial 10-year mine life. The second cornerstone royalty is a 2% NSR royalty, acquired in February 2021, from South 32, on Karlawinda Gold Project, Australia's newest mine scheduled to have first gold pour in Q2, 2021.

Elemental Royalties Corp.

Dr. Allen Alper:

This is Dr. Allen Alper, Editor-in-Chief of Metals News, talking with Frederick Bell, who is CEO and Director of Elemental Royalties. Frederick, could you give our readers/investors an overview of your Company and what differentiates your Company from others?

Frederick Bell:

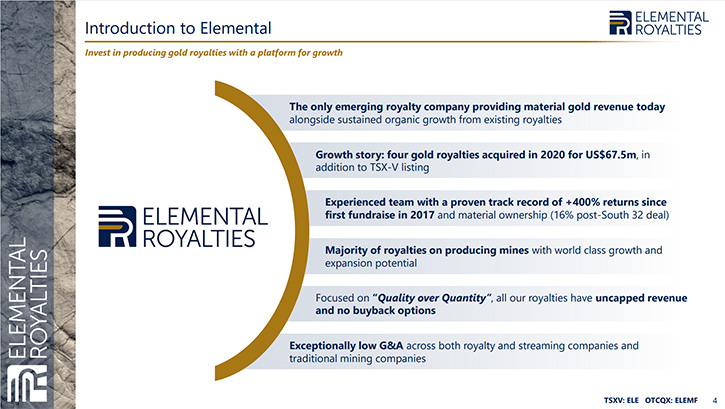

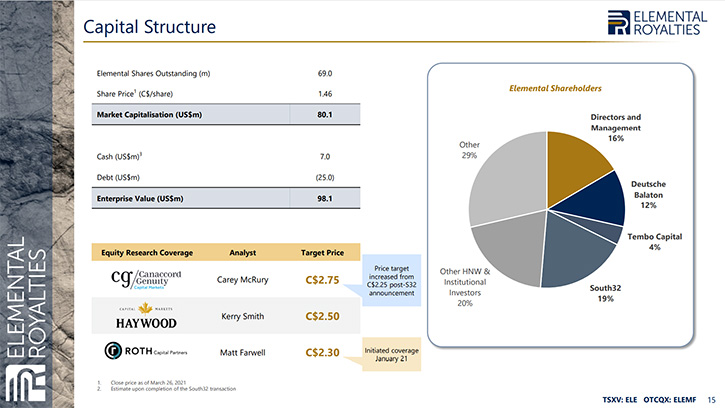

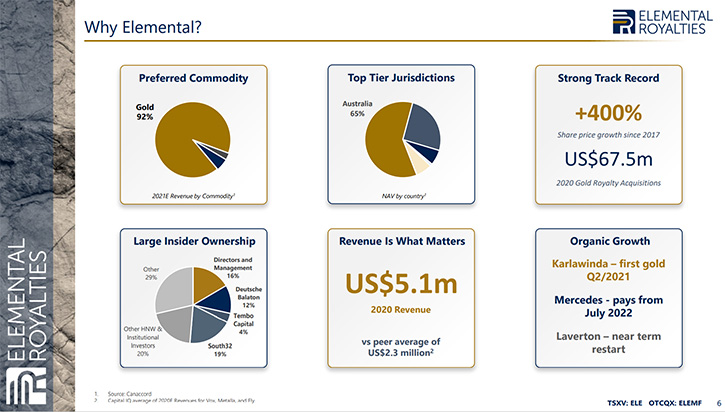

I think Elemental is best summed up by the fact that our portfolio is predominantly precious metals royalties. For a roughly 100 million market cap, Canadian Company, I think that is probably the thing that differentiates us most in the space. I suppose the ultimate goals of a royalty company are to have diversified revenue cash flow, from different assets. We've had cash flow from day one, as a company, we listed on the TSX-V in 2020 in Canada. As of today, we have a portfolio of nine royalties and revenue from a number of assets, different operators, different companies. That's really important because we have all the growth of a small royalty company to grow, and we have nearly doubled our revenue year on year, but we also have the downside protection of revenue from independent, different good quality assets.

Dr. Allen Alper:

Sounds excellent. Could you tell our readers/investors about your royalty portfolio?

Frederick Bell:

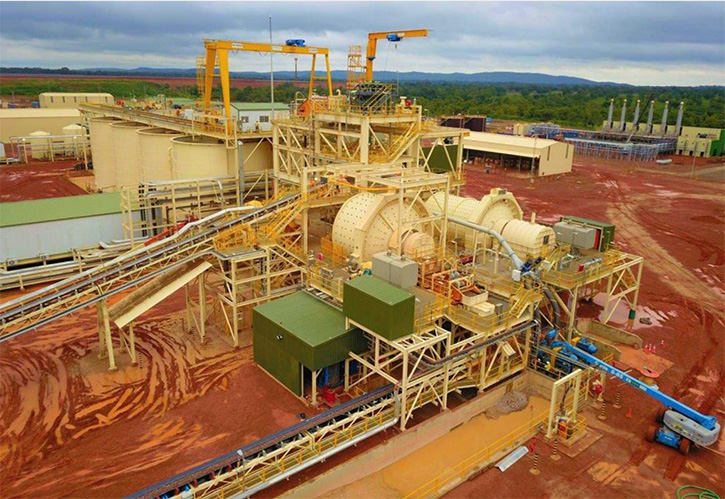

One of the areas that we really focus on is keeping good quality assets. A lot of projects can take five, 10 years to be taken from exploration through to development and production. We have some really good quality producing operating mines, from which we have royalties. The current biggest revenue earner is a royalty, owned by Endeavor Mining, for top 10 gold producers globally. It did 175,000 ounces last year, which was its first full year of production, it's a new mine and we have a 1% royalty over the whole thousand square kilometer license package.

That is a mine that Endeavor announced $12 million of exploration on this year, and we think it will have a really long life and be a cornerstone asset for us. Our second cornerstone asset is a royalty we just acquired, the deal closed in February 2021, in a portfolio of royalties we acquired from South 32, who are spun out from BHP, the world's largest mining company. That royalty is Australia's newest mine and it is scheduled to have first gold core in Q2, 2021. Once that royalty comes on, that will be our largest revenue earner. It is a 2% royalty on a roughly 120,000 ounce a year mine.

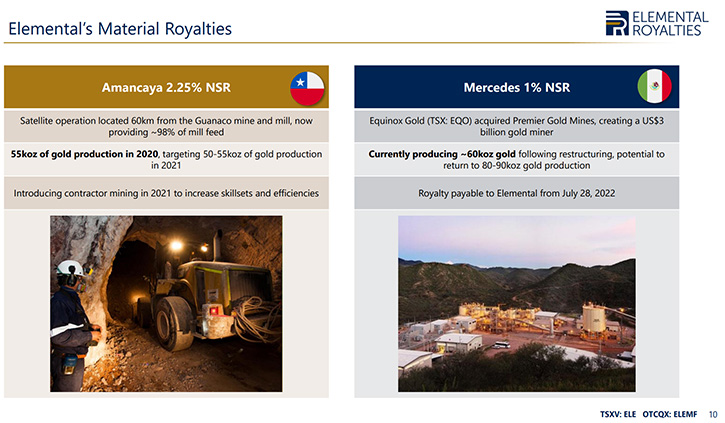

The key thing, with it, is it's a very well known, successful Management Team in Australia, and it is a mine that starts with a 10 plus years reserve life. We see great exploration potential for that to keep growing, at no cost to us, as a royalty holder. Those are two of our really big material, cornerstone assets. I think one or two others are worth mentioning, like The Mercedes Mine that Equinox Gold just acquired, through the acquisition of Premier Gold. We have a 1% royalty on the 700 square kilometer license. That starts paying us from the middle of next year. Our largest percentage royalty, 2.25% on Austral Gold's Amancaya Mine in Chile is an operating asset as well.

That doesn't cover all of them. But it gives you a flavor of some of the assets we have. These are not speculative exploration assets. These are operating mines, with a history of production, a history and a track record of mining exploration success as well, adding new ounces. And to have that in a 100 million market cap royalty company, I think is what sets us apart from anyone else.

Dr. Allen Alper:

Well, those are very impressive royalties that you have, and you've accomplished an amazing amount in a very short time. Could you tell our readers/investors a little bit about your background and your team?

Frederick Bell:Elemental was a startup royalty company in every sense, this was just a good idea four years ago. Our first royalty acquisition we acquired from Acacia, which is now part of Barrick Gold. It was a $2 million deal and we had to give away half of it to a private equity fund in order to get the company started. We started this from the ground up. I think building this all the way through has given us a lot of advantages because we've had to do it all the hard way. If you look at where we are from, when we started in 2017, that deal was a million-dollar acquisition.

Our last acquisition was a $55 million acquisition. If you look at our share price, we were approximately 27 cents and we're about $1.50 now, we've been able to grow the Company and we've almost doubled the revenue year on year. We have increased the share price every time we have raised money. Doing that, it gives you an awful lot of experience and knowledge in the royalty space. We've now acquired royalties on three different continents, from a number of different operators and counter parties, including Acacia, including Yamana Gold, most recently with South 32 and they're a $10 billion market cap. That latest acquisition became our largest shareholder and they have appointed a Director on the Board as well.

That speaks to the value that they see in the Company and what we can deliver going forward. We have a core Management Team that is mid-thirties in age. Around us, we have some really good experience and we're part of Discovery Group in Canada, with John Robins and Jim Patterson and that's had some really good successes, a good track record and is very well known in Canada. Richard and Peter, both from Australia, worked for Western Mining before it was taken over by BHP. They are geologists and geophysicists by background. I think what it means is we have a really motivated, driven team in their 30s, but with all the experience and technical backgrounds and contacts and network that comes from having some of the more experienced Board and Management around.

Dr. Allen Alper:

That sounds excellent! That's a great Team and you have great backing, with the Discovery Group. That's excellent! Could you tell our readers/investors a little bit about your capital and share structure?

Frederick Bell:

We have 69 million shares outstanding. There are no warrants. We have never issued a warrant in the history of the Company. The only options are to Management and Directors. As of today, the Management and Directors own about 16% percent of the Company. South 32, with the last acquisition, has about 19% percent. There are a couple of institutions and private shareholders, who probably own about 30% percent among them. It's a pretty tightly held capital structure.

In terms of our cash, at the moment, we have about $7 million US. We used an acquisition facility, with the last transaction of $25 million US that we drew down. That's one of the benefits, as you grow a royalty company, with producing royalties, you can start to borrow to build out your portfolio, instead of diluting shareholders.

I think that is something that, as we get increasingly larger, our borrowing costs come down. I think that's something that really speaks to the quality of our assets, because not a lot of companies can do it. We have some really good quality institutional shareholders, which is unusual for a Company of our size. We've been able to access credit, which again, is pretty unusual for a Company of our size. The quality of assets that we have are cash flowing. We have been cash flow positive from day one, with the ability to access more capital and debt and have about $7 million in the bank.

Dr. Allen Alper:

That sounds excellent and it's good to see that Management has skin in the game and is confident in the future of the Company.

Frederick Bell:

In the last financing we did, for the South 32 acquisition, maybe it was a $1.50 price, which is similar to where we are today. I think Management and Directors probably put a million dollars plus into that financing. We have invested in every round and I think that's really important, because it guides how we make our decisions. We need to succeed by getting the share price up rather than anything else.

Dr. Allen Alper:

That sounds excellent. Could you tell us just what are your primary goals for 2021?

Frederick Bell:

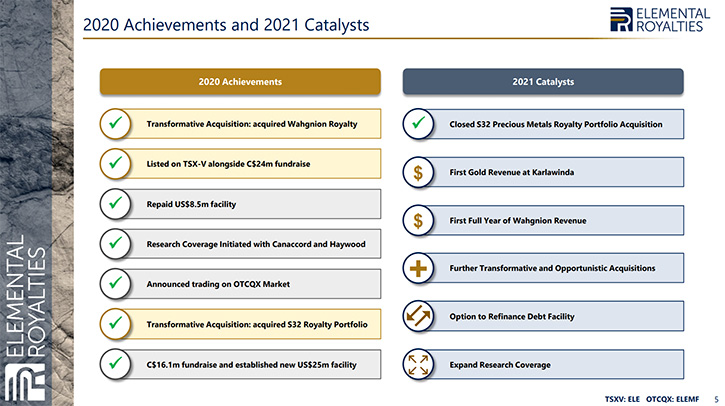

The biggest catalyst is Karlawinda Royalty that is under construction as First Gold, targeted for June. I think that coming on stream will put us in a very different position going forward. Three of our key assets, Karlawinda, Wahgnion, and Laverton have all announced reserve and resource updates that I think are expected in 2021. That's really positive for us, because in the royalty space, where you really do well is when they find more on your projects and you don't have to pay for it. To have all three of those companies actively exploring and adding value will really start to show in the second half of this year.

We are looking at options to refinance the debt facility, with some of the bigger Canadian banks and it speaks to the maturity of the royalty company when you can do that. Currently in the sub billion-dollar royalty space, there are two companies that have done it. I think if we can do that in the second half of this year as a currently $100 million market cap company, it will distinguish us and it will differentiate us from peers who haven't been able to do that yet.

The last point is just that we have organic growth royalty revenue in our portfolio. We have, in the first year, 12 months of royal revenue from Wahgnion. Next year will be the first year that we have a full 12 months of royalty revenue from Karlawinda and in 2023, it will be the first year that we have a full year revenue from Mercedes, which is already an operating line. You have 100% revenue growth already in the portfolio, already in what we own, but none of it really reflected in the valuation in the current sharp rise. I think that's a great position to be on. These are development projects, which could be delayed by two years. The earlier stage one is due to have its Gold pour in Q2. It's had the best revenue growth. I think that's something that as a royalty company, we can look forward to even if we do nothing else over the next year. That's the benefit of the model, every new acquisition we make, we layer on more growth, we layer on more assets, and we add value each time.

Dr. Allen Alper:

Well, that's really excellent! 2021will be an extremely exciting time for Elemental Royalties and their stakeholders and shareholders.

Frederick Bell:

It will be our first year as a listed company, although we've been around for a few years, every quarter that goes by is another quarter that we can point to a performance track record, it's public what we've done. I think that that will really help because at the moment, since we listed the company publicly, we haven't been able to come to Canada, we haven't been able to come to the US, we haven't met some of our shareholders. Over the course of 2021, if that becomes possible and we can raise our profile, it will be positive.

Dr. Allen Alper:

That sounds excellent. Frederick, could you highlight and summarize the primary reasons our readers/investors should consider investing in the Elemental Royalties?

Frederick Bell:

The fundamental reason we set up Elemental, was to give investors an opportunity to get exposure to gold and to do it with an asymmetric risk profile. At this stage in the company's evolution, we're still only a few years old, but you can get exposure to multiple different operating mines, different countries, different jurisdictions, different companies that run them. You have a much lower risk profile than you do in a single asset developer explorer.

The other great benefit you have is that, at the moment, our costs are very low because we're not running any assets, we're not operating as mines. We're past the risky stage. Where we sit today, with very limited downside, we've shown and proven that we've been able to grow the company, doubling the revenue year on year. We already have a lot of growth, more than we've ever had before or in the company's portfolio.

If you look at us today, what's the downside risk? Well, it's limited because you have revenue coming in from multiple different assets, good quality assets that are adding ounces, adding mine life. What's the upside? Well, we know that we already have about 100% upside in terms of revenue over the next year, even if we do nothing else. In the history of the Company, we've never done anything else, we've always been able to grow it and build on it. I think it's a pretty unique risk profile. There's not a lot of downside and there's an awful lot of upside, even if we were locked up in the next year and not able to do anything.

Dr. Allen Alper:

Well, all very strong, compelling reasons for investors to consider investing in Elemental Royalties.

https://www.elementalroyalties.com/

Frederick Bell

CEO and Director

info@elementalroyalties.com

|

|