|

|

|

|

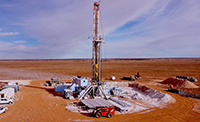

Prospect Ridge Resources Mining Exploration in B.C.'s Bowser Lake and Hazelton Groups Rock Geology

by SmallCapInterviews

With multiple M&A activities in Canada's Northern British Columbia in 2023, mining activity in B.C. is heating up, especially in regions containing Bowser Lake Group and Hazelton Group rock geology. Bringing their long history of success in the mining industry, our next guests have a new B.C. mining project that has caught their attention. Prospect Ridge Resources' new CEO Michael Iverson and President Yan Ducharme discuss what compelled them to join their latest exploration venture searching for gold, copper and silver just south, outside British Columbia's Golden Triangle.

Click here to continue... |

Steve Hanson, President and CEO, ACME Lithium Inc. (CSE: ACME, OTCQX: ACLHF) Discusses their Planning for a Domestic Supply of Lithium for Powering the Energy Revolution

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Steve Hanson, President and CEO of ACME Lithium Inc. (CSE: ACME, OTCQX: ACLHF), a mineral exploration Company, with multiple North American projects, in areas known for lithium development and exploration. ACME has acquired, or is under option to acquire, a 100-per-cent interest in projects, located in Clayton Valley and Fish Lake Valley, Esmeralda County Nevada, and at Cat-Euclid and Shatford Lakes, in southeastern Manitoba. The claims translate to lithium mining and extraction, in a growing market that is set to dominate in the coming years. The summer drilling program, in Nevada, produced a significant discovery, with Lithium detected at concentrations ranging between 38 and 130 mg/L. These findings have initiated Phase 2 planning and procurement of an expanded drilling and pump test program, with a target to commence Q4 2022. In Manitoba, drilling is planned for Fall-Winter 2022-2023, based on findings from the summer exploration program.

Click here to continue... |

Interview with Gary Thompson, Chairman, CEO, President and P.Geo., Brixton Metals Corporation (TSX-V: BBB, OTCQB: BBBXF): A Huge District Scale Copper-Gold-Silver-Molybdenum Project in British Columbia

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Gary Thompson, Chairman, CEO and President, and Professional Geologist of Brixton Metals Corporation (TSX-V: BBB, OTCQB: BBBXF) a Canadian exploration Company, focused on their flagship, Thorn Copper-Gold-Silver-Molybdenum Project (a major porphyry district). The Company’s other project, which includes the Hog Heaven Silver-Gold-Copper Project, in NW Montana, USA (under option to Ivanhoe Electric Inc., NYSE: IE), the Atlin Goldfields Projects, located in NW BC, (under option to Pacific Bay Minerals Ltd., TSXV: PBM) and the Langis-HudBay Silver-Cobalt-Nickel Projects, in Ontario. Brixton has recently secured a strategic investment from BHP Group Limited, with the goal of advancing the Thorn Project. The wholly owned, 2,863 square kilometer Thorn Project is located in Northwestern British Columbia, at the northern extension of the prolific Golden Triangle, Canada, approximately 90 km northeast of Juneau, AK, and about 50 km from tide water. Fourteen large-scale copper-gold targets have been identified on the project, to date, that warrant further exploration work.

Click here to continue... |

Gregg Smith, President & CEO and Greg Phaneuf, VP Finance & CFO, Grounded Lithium Corp. (GLC): Discuss their Vision to Become a Canadian Lithium Producer, Supporting the Global Energy Transition

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Gregg Smith, President and CEO and Greg Phaneuf, VP Finance and CFO of Grounded Lithium Corp. (GLC), a private lithium brine exploration and development Company, with a vision to build a best-in-class, environmentally responsible, Canadian lithium producer, supporting the global energy transition shift. GLC targets and controls lands, that will support multiple 20,000 tonnes/year projects. GLC's Kindersley Lithium project has an inferred resource of 2.9M tonnes LCE. GLC intends to utilize a direct lithium extraction (DLE), in its production of battery-grade lithium carbonate equivalent, or lithium hydroxide, depending on customer preferences, an ESG-friendly process that; minimizes capital costs, reduces permitting risks and allows for faster production, with higher recoveries. Near term plans include; concentration testing, extraction testing, deliverability test results from GLC’s well, drilled in August 2022, lab pilot, additional test results from GLC proprietary wells, in addition to access to legacy oil and gas wells, and a PEA in Q3 2023.

Click here to continue... |

Colin Moorhead, Executive Chairman and MD, Xanadu Mines (ASX: XAM, TSX: XAM), Discusses Their Gold-rich Copper Exploration in Mongolia and Its Potential as One of the Last Great Copper Frontiers

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Colin Moorhead, who's Executive Chairman and Managing Director of Xanadu Mines (ASX: XAM, TSX: XAM), a company that discovers, defines, and develops globally significant porphyry copper-gold deposits, in Mongolia. The Company owns a multi-stage portfolio of projects, with the flagship Kharmagtai copper-gold project, located in Omnogovi Province, approximately 420km southeast of Ulaanbaatar, within the South Gobi porphyry copper province, which hosts most of the known porphyry deposits, in the South Gobi region of Mongolia. The project has a mineral resource estimate of 1.1Bt, with 3Mt Cu & 8Moz Au, including higher-grade core of 100Mt, grading 0.8% Cu Eq. A recent scoping study shows US$630M NPV (405-850); 20% IRR (16-25%); 4-year payback (4-7). Kharmagtai is fully funded towards a decision to construct, via strategic partnership, with Zijin Mining. Around a month ago, Xanadu kicked off a new exploration program, at their 100% owned Red Mountain project; seeking to expand strike extent of shallow, high-grade epithermal gold & copper-gold-silver skarn mineralisation. For Kharmagtai, near-term plans include a Pre-Feasibility Study (PFS) commencing Q1 CY2023, along with a reinvigorated discovery exploration program, focused on higher-grade targets.

Click here to continue... |

Marc Roy, CEO, Focus Graphite Inc. (TSX.V: FMS; OTCQX: FCSMF; FRANKFURT: FKC) Discusses Providing a Steady Secure Supply of Graphite to Feed the Green Energy Revolution

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Marc Roy, who is CEO of Focus Graphite Inc. (TSX.V: FMS; OTCQX: FCSMF; FRANKFURT: FKC), a technology-oriented exploration and development company that seeks to produce flake graphite concentrate at its wholly owned Lac Knife and Lac Tétépisca flake graphite projects, located in the Côte-Nord administrative region of Québec. As part of its mission to build long-term, sustainable shareholder value, Focus is also evaluating the feasibility of producing value-added specialty graphite products, including battery-grade spherical graphite. Near-term plans include updating of the feasibility study at Lac Knife, as well as drilling at Lac Tétépisca and moving the project to the PEA stage. Focus also holds an equity position in graphene applications developer, Grafoid Inc.

Click here to continue... |

Ron Thiessen, President & CEO, Northern Dynasty Minerals Ltd. (TSX: NDM; NYSE American: NAK) Discusses the Need for their Pebble Project to Supply Copper for Electrification and Green Energy

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Ron Thiessen, President, and CEO of Northern Dynasty Minerals Ltd. (TSX: NDM; NYSE American: NAK), a Canadian mineral exploration and development company. Northern Dynasty is focused on their principal asset, the world class copper/gold/silver/moly/rhenium Pebble Project, owned through its wholly owned Alaska-based U.S. subsidiary, Pebble Limited Partnership. The project is located in southwest Alaska about 200 miles from Anchorage and 125 miles from Bristol Bay. The Pebble Project's 2021 PEA is financially robust and combines globally significant production and excellent optionality. The ability of Pebble to produce copper at a low cash cost and generate many millions in annual taxes and other government revenues in Alaska, while setting aside appropriate closure funding, could propel this region of Alaska into prosperity and opportunity. In 2020, the project permit was denied, and in early 2021, Pebble lodged an Administrative Appeal against the decision, which continues today.

Click here to continue... |

Interview with Garrett Ainsworth, President and CEO, District Metals Corp. (TSX-V: DMX, FRA: DFPP): Exploring for Rich Polymetallic Deposits in a World Class Mining District: Bergslagen, Sweden

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Garrett Ainsworth, who is President and CEO of District Metals Corp. (TSX-V: DMX, FRA: DFPP), a geoscience-based, systematic, and valuation-oriented exploration and development Company, focused on the world class mining district, of Bergslagen, Sweden. The Company's flagship is the advanced exploration stage, polymetallic Tomtebo Property that comprises 5,144 ha and is situated between two significant historic polymetallic mines, with numerous polymetallic mines and showings, along an approximate 17 km trend that exhibits similar geology, structure, alteration and VMS/SedEx style mineralization, as other significant mines within the district. The maiden drill program, at the polymetallic Gruvberget Property, completed in July 2022, has been a great success, and returned significant polymetallic assays, over appreciable widths, with continuity that remains open, from a shallow vertical depth of approximately 160 m. District Metals plans to conduct their next drilling programs in 2023.

Click here to continue... |

Peter Schloo, President, CEO and Director, Heritage Mining, Ltd. (CSE: HML) Discuses Exploring High Grade, Gold and Copper, District-Scale, Drayton-Black Lake Flagship Project in Ontario

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Peter Schloo, President, CEO and Director of Heritage Mining, Ltd. (CSE: HML), a new junior mineral exploration Company that went public on August 26, 2022. The Company's, district-scale, Drayton-Black Lake flagship project totals ~15,256Ha, in northwestern Ontario, Canada. The project is on trend, with Treasury Metals’ (Goliath Complex), with multiple, high-grade, gold and copper occurrences. There are several, well-defined, near-term drill targets, over four zones, close proximity to infrastructure, combined with over 100 years of exploration data (176 historic DDH totaling ~20km) never compiled until 2022. Heritage Mining is well capitalized, with a tight Capital structure, with approximately 31.9M common shares outstanding. The Company’s Veteran Board and Management Team has over 100 years of experience in the mining and exploration industry, with a proven track record.

Click here to continue... |

Interview with Canadian Mining Hall of Fame Recipient Dr. Robert Quartermain, Co-Chairman and Jonathan Awde, President & CEO, Dakota Gold (NYSE American: DC): New Gold Discoveries, Covering over 40 Thousand Acres, Surrounding the Historic Homestake Mine, South Dakota

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with, Dr. Robert Quartermain, who is Co-Chairman, and Jonathan Awde, who is President and CEO of Dakota Gold (NYSE American: DC). Dakota Gold is a South Dakota-based, responsible gold exploration and development company, with a specific focus on revitalizing the Homestake District in Lead, South Dakota. Dakota Gold is focused on new gold discoveries, and has high-caliber gold mineral properties, covering over 40 thousand acres, surrounding the historic Homestake Mine. In 2020, Dakota Gold made an agreement with Barrick Gold Corporation, which includes Maitland Gold Project purchase, the three-year surface Barrick option agreement, and the three-year Richmond Hill option agreement. Today the Company is aggressively exploring and working on community integration.

Click here to continue... |

Interview with Caleb Stroup, President and CEO, Headwater Gold, Inc. (CSE: HWG, OTCQB: HWAUF): Technical and Discovery-Oriented Team, Exploring and Discovering High-Grade Precious Metal in Western USA

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Caleb Stroup, President and CEO of Headwater Gold, Inc. (CSE: HWG, OTCQB: HWAUF), a technically driven, discovery-oriented, mineral exploration Company, focused on the exploration and discovery of high-grade precious metal deposits, in the Western USA. Headwater has a large portfolio, of epithermal vein exploration projects, and a technical Team, comprised of experienced geologists, with diverse capital markets, junior company, and major mining company experience. The Company is systematically drill testing several projects, in Nevada, Idaho, and Oregon. Headwater raised $4 million and listed, in June, this year. Headwater drilled four projects, right in sequence and had two new discoveries, one at their Katey Project, along the Oregon-Idaho border, and one at their Spring Peak Project, in Nevada. The Company attracted Newcrest Mining Limited and partnered, with them, on the new exploration program, on 2 of the four projects.

Click here to continue... |

Elixir Energy (ASX: EXR): Coal Bed Methane (CBM), Very Large Asset in Mongolia’s South Gobi Region, Excellent Infrastructure, Close to Rapidly Growing Chinese Gas Market; Neil Young, MD Interviewed

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

Elixir Energy (ASX: EXR) holds a 100% interest, in the Nomgon IX coal bed methane (CBM) production sharing contract (PSC), a very large asset, located proximate to the Chinese border, in Mongolia’s South Gobi region, near excellent infrastructure, and close to the rapidly growing Chinese gas market. The PSC has a minimum ten-year exploration period and a thirty-year (extendable) production period. We learned from Neil Young, Managing Director of Elixir Energy, that in the course of 2020, they successfully undertook exploration and appraisal work on the PSC, including drilling several holes, seismic acquisition and geological survey work, with results that meet or exceed those of a number of producing CSG fields, around the world.

Click here to continue... |

Anthony McClure, Managing Director, Silver Mines Ltd (ASX: SVL) Discusses their Bowdens Silver Project, the Largest Undeveloped Silver Deposit in Australia and One of the Largest Globally

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Mr. Anthony McClure, who is Managing Director of Silver Mines Limited (ASX:SVL), an Australian mineral exploration and development company that owns the Bowdens Silver Project located near Mudgee, in New South Wales. Previously held by Silver Standard, Bowdens Silver is the largest undeveloped silver deposit in Australia and one of the largest globally. It contains substantial resources, and boasts outstanding logistics, for future mine development. Considerable body of high-quality technical work has already been completed. The project has had continued outstanding high-grade drilling results, and drilling will go on through 2022. Resource assessment and Scoping Study for a potential underground development commenced for completion in 2022.

Click here to continue... |

John Cash, Chairman, CEO and President, Ur-Energy Inc. (NYSE American: URG), Discusses Supplying Uranium for Green Energy, with their Growing Low-Cost Uranium Mining Company, in Wyoming, USA

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with John Cash, Chairman, CEO and President of Ur-Energy Inc. (NYSE American: URG), a uranium mining company, operating their low-cost, Lost Creek, in-situ recovery, uranium facility in south-central Wyoming. Ur-Energy has produced, packaged, and shipped approximately 2.6 million pounds of U3O8 from Lost Creek, since the commencement of operations. Ur-Energy has all major permits and authorizations to begin construction at Shirley Basin, the Company's second in situ recovery uranium facility, in Wyoming and is in the process of obtaining remaining amendments to authorizations for expansion of Lost Creek. According to Ur-Energy, the recovery of Lost Creek and Shirley Basin resources will offset ~312.4M metric tons CO2 compared to coal power, which is equivalent to taking 67.5 million cars off the road for a year.

Click here to continue... |

Dev Randhawa, Chairman & CEO and Raymond Ashley, P.Geo., Fission 3.0 Corp. (TSXV: FUU, OTCQB: FISOF) Discuss Exploring for High-Grade Uranium in the Premier Athabasca District, World Class Team

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Dev Randhawa, Chairman and CEO and Raymond Ashley, Professional Geoscientist of Fission 3.0 Corp. (TSXV: FUU, OTCQB: FISOF), a uranium project generator and exploration company, focusing on projects in the Athabasca Basin, home to some of the world's largest high-grade uranium discoveries. Fission 3 currently has 16 projects in the Athabasca Basin. Several of Fission 3's projects are near large uranium discoveries, including, Arrow, Triple R and Hurricane deposits. The extensive 2022 Summer exploration work program included drilling at Lazy Edward Bay and Murphy Lake. Prospecting, sampling, and ground geophysics are also planned at Hearty Bay to ready the property for follow up drilling next winter. The PLN property is the most advanced, of the Fission 3 portfolio, by virtue of its proximity to the world class uranium deposits, being advanced by Fission Uranium Corp and NexGen. A 3000m drilling program is planned at PLN property in the fall.

Click here to continue... |

|

Jason Beckton, Managing Director, Prospech, Ltd. (ASX: PRS), discusses their Under Explored, Gold and Silver Exploration Licenses, in the Tethyan Magmatic Arc, in Slovakia, One of the Most Prolific Global Metal Belts

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Jason Beckton, who is Managing Director of Prospech, Ltd. (ASX: PRS). Prospech owns 100% of 204km² of prospective, under explored, gold and silver exploration licenses, in the Tethyan magmatic arc, in Slovakia, which is one of the most prolific global metal belts. The Company has recently made a new discovery, at the Low Angle Normal Fault (LANF) prospect, at their historic Hodrusa-Hamre project. Drilling was conducted at the LANF targets and Schopfer prospect this summer, and Prospech is currently receiving the results. In addition, in September, the new exploration licence has been applied for and granted at the Kolba cobalt-copper-nickel property, located in Central Slovakia, proximate to the Company’s existing operations. Slovakia is an advanced economy, with producing mines and is a member of the European Union and Eurozone.

Click here to continue... |

Interview with Rob McEwen, Chief Owner and Chairman, McEwen Mining Inc. (NYSE: MUX, TSX: MUX): Discusses Outlook for Gold, Silver and Copper and his Goals for McEwen Mining

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Rob McEwen, Chief Owner and Chairman of McEwen Mining Inc. (NYSE: MUX, TSX: MUX), a diversified gold, silver producer and explorer, focused on the Americas, with operating mines in Nevada, Canada and Argentina. In addition, owning 68% of McEwen Copper, which owns a 100% of the Los Azules copper project, in San Juan Province, Argentina and it owns 100% of the Elder Creek project, in Nevada, USA. Los Azules is located in one of the most significant copper districts globally and is considered to be the 9th largest, undeveloped copper project, in the world. According to the project’s Preliminary Economic Assessment (PEA), completed in 2017, during the first 10 years of the 36 years of operations, the project is anticipated to be one of the world's larger copper producers, with costs in the lowest quartile. Near-term plans include further metallurgical, geotechnical & hydrology programs and drilling to support an updated PEA, to be released in Q1, 2023, in preparation for an IPO in Q2, 2023.

Click here to continue... |

Interview with Kyle Floyd, CEO, Vox Royalty Corp. (NASDAQ: VOXR, TSXV: VOX): A data driven, returns focused, Royalty Company

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Kyle Floyd, CEO of Vox Royalty Corp. (NASDAQ: VOXR, TSXV: VOX), a returns focused, mining royalty company established in 2014, with a portfolio of over 50 royalties and streams, spanning eight jurisdictions. Vox’s portfolio is predominantly weighted towards precious metals royalties, which make up over 70% of its portfolio weighting by NAV. In addition to the precious metals’ royalties, the Company has underlying exposure to a more diverse array of commodities, including base and battery metals and certain bulk commodities. Vox's portfolio spans four continents, but is heavily weighted to Australia and North America, where >80% of their assets are located. Vox has both immediate cash-flowing royalties, generating recurring revenue and royalties, over several long-life, economically robust development-stage assets, with great operating counterparties. Since the beginning of 2020, Vox has announced over 20 separate transactions, to acquire over 50 royalties.

Click here to continue... |

Dr. Dave R. Webb, President and CEO, Sixty North Gold Mining, Ltd. Discusses High-Grade Gold Mining: Restarting a Past Producing Gold Mine within the Prolific Yellowknife Gold Camp, NWT

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Dr. Dave R. Webb, President and CEO of Sixty North Gold Mining, Ltd. (CSE: SXTY, FKT: 2F4, OTC-Pink: SXNTF), who are focused on restarting the high-grade, past producing, Mon Mine, 40 km north of Yellowknife, NWT, within the prolific Yellowknife Gold Camp. The Mon Mine produced 15,000 ounces of gold, from 15,000 tonnes of ore, between 1989 and 1997. Permits to explore, mine and mill, at 100 tpd, are in place, and the Mon Mine is the only gold project permitted for production, in the NWT. Sixty North Gold is expecting to commence its mill and mine operations in Q2 2023. It expects the first cash receipts, from gravity gold sales, to come in Q3 2023. Other targets on the property include recently discovered silver-and gold-rich VMS targets, as well as the giant shear zone-hosted gold mineralization. Recently, the Company made an unexpected, brand-new, high-grade, Nickel-Cobalt-PGM discovery, on the property, which is the first reported nickel showing in the Yellowknife Gold Belt.

Click here to continue... |

Abraham Drost, P. Geo and CEO and Director of Clean Air Metals Inc. (TSXV: AIR, OTCQB: CLRMF, FRA: CKU) Discusses Exploring and Developing the High-Grade Thunder Bay North Platinum, Palladium, Copper, and Nickel Project in Ontario

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Abraham Drost, who's a professional geologist and CEO and Director of Clean Air Metals Inc. (TSXV: AIR, FRA: CKU, OTCQB: CLRMF). Clean Air Metals' flagship asset is the 100% owned, high grade Thunder Bay North platinum, palladium, copper, and nickel project, located near the City of Thunder Bay, Ontario and the Lac des Iles Mine, owned by Impala Platinum. The robust PEA, filed January 12, 2022, highlights a solid foundation, with a 10-year mine life, a processing rate of 3,600 tpd, LOM average operating cash cost of $86.61 per tonne, $536.4 million in total capital costs, pre-tax NPV 5% of $425.0 million and IRR of 31.1%, total revenue of C$ 2,244.8 million, and initial payback period (pre-tax) of 2.4 years. Near-term plans include completing prefeasibility studies in Q2 2023, for a low-carbon, all-electric sustainable mining operation, at Thunder Bay North. The construction decision is expected in Q4 2024.

Click here to continue... |

Interview with David Williams, Executive Chairman, Thomson Resources (ASX: TMZ, OTCQB: TMZRF): Rapidly Advancing the New England Silver District into Production

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with David Williams, who's Executive Chairman of Thomson Resources (ASX: TMZ, OTCQB: TMZRF). Thomson Resources has aggressively consolidated a large precious (silver – gold), base and technology metal (zinc, lead, copper, tin) resource hub called “New England Fold Belt Hub and Spoke", that could be developed and potentially centrally processed. The Company's strategy is underpinned by its diverse portfolio of tenements across gold, silver and tin, in New South Wales and Queensland. These projects include the Webbs and Conrad Silver Projects, Texas Silver Project, and Silver Spur Silver Project, as well as the Mt Carrington Gold-Silver earn-in and JV. As part of its New England Fold Belt Hub and Spoke Strategy, Thomson is targeting, in aggregate, inground material available to a central processing facility of 100 million ounces of silver equivalent.

Click here to continue... |

Interview with Donald Bubar, P.Geo. and CEO, Avalon Advanced Materials Inc. (TSX: AVL, OTCQB: AVLNF): Uniquely Positioned for Supplying Lithium Battery Materials and the rare lithium mineral, Petalite, for high-strength Glass-Ceramic Manufacturers

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Donald Bubar, who is a Professional Geologist and CEO of Avalon Advanced Materials Inc. (TSX: AVL, OTCQB: AVLNF), a Canadian mineral development company, specializing in sustainably produced materials, for clean technology. The Company now has four advanced stage projects, providing investors with exposure to; lithium, tin and indium, as well as rare earth elements; tantalum, cesium and zirconium. Avalon is currently focusing on developing its Separation Rapids Lithium Project near Kenora, Ontario, while continuing to advance other projects, including its 100%-owned Lilypad Cesium-Tantalum-Lithium Project located near Fort Hope, Ontario. The Company has just announced that they entered into an off-take agreement, for petalite concentrates, from a major, non-Chinese, international glass-ceramics manufacturer. There is now considerable interest from other major glass ceramic manufacturers, in Europe and Asia, as there is presently a global shortage of petalite supply, after China took control of the traditional petalite supply sources in Zimbabwe.

Click here to continue... |

Interview of Eric Zaunscherb, Chairman & CEO, GR Silver Mining (TSXV|GRSL, OTCQB|GRSLF, FRANKFURT|GPE): District-Scale Silver and Gold Portfolio and Resource Expansion in a Prolific Mining District in Mexico

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Eric Zaunscherb, Chairman and CEO of GR Silver Mining Ltd. (TSXV|GRSL, OTCQB|GRSLF, FRANKFURT|GPE), a Canadian-based, Mexico-focused, junior mineral exploration company, engaged in cost effective silver-gold resource expansion, on its 100%-owned assets, located on the eastern edge of the Rosario Mining District, in the southeast of Sinaloa State, Mexico. GR Silver Mining controls 100% of two past producers, precious metal underground and open pit mines, within the expanded Plomosas Project, which includes the integrated San Marcial Area and La Trinidad acquisition. In conjunction with a portfolio of early to advanced stage exploration targets, the Company holds 734 km2 of concessions, containing several structural corridors, totaling over 75 km, in strike length. The recent drilling results include Drill Hole 22-10, which intersected 101.6 meters at 308 grams per tonne silver, from 98.5 meters downhole.

Click here to continue... |

SPC Nickel Corp. (TSX-V:SPC) : Discovering Class 1 Nickel in a World Class Mining Camp; Interview with Grant Mourre, President and CEO

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Grant Mourre, President, and CEO of SPC Nickel Corp. (TSX-V:SPC), a Canadian public corporation, focused on exploring for Ni-Cu-PGMs, within the world class Sudbury Mining Camp. The Company is currently exploring its key, 100% owned, exploration projects, Lockerby East, and Aer-Kidd, both located in the heart of the historic Sudbury Mining Camp and adjacent to producing mines, past producing mines, or development projects. The fully funded, 2022 exploration program is underway and includes diamond drilling at Lockerby East that should provide steady news flow. SPC Nickel is also planning exploration activities, on its two other projects, the Muskox Property, located in Nunavut, and the Janes Ni-Cu-PGM Property, located approximately 50 km northeast of Sudbury.

Click here to continue... |

Rick Van Nieuwenhuyse, President, and CEO, Contango ORE, Inc. (NYSE American: CTGO) Discusses Developing the Highest-Grade Open Pit Gold Mine in the World, Partnered with Kinross

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Rick Van Nieuwenhuyse, President, and CEO of Contango ORE, Inc. (NYSE American: CTGO), a well-capitalized US gold developer, with a clear path to producing, on average, 67,500 GEO/year, with Kinross guidance all-in sustaining costs of $900 gold equivalent ounces for the Manh Choh deposit. The Company's flagship Manh Choh project, located on the Alaska Hwy on private land owned by the Tetlin Alaska Native Tribe, is the development stage project, under construction, in partnership with Kinross (70%) and the Alaska Native Tetlin Tribe (Royalty). The project holds approximately 1 million ounces of gold in measured and indicated resources, at an average grade of 8g/t gold, which is going to be mined over a 4.5 year mine-life starting early 2024. The Manh Choh ore will be trucked and processed at Kinross’ Fort Knox Mill, resulting in lower capital costs, a smaller environmental footprint and lower execution risk.

Click here to continue... |

Interview with Don Mosher, President, Desert Mountain Energy Corp. (TSX.V: DME, U.S. OTC: DMEHF, Frankfurt: QM01): Building North America's First Vertically Integrated, Primary Producer of Helium

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Don Mosher, President, and Director of Desert Mountain Energy Corp. (TSX.V: DME, U.S. OTC: DMEHF, Frankfurt: QM01), a forward-looking resource company, actively engaged in the exploration and development of Helium and Noble Gas, at their wholly owned, district-scale Holbrook Project, in Arizona’s Holbrook Basin. Desert Mountain Energy is advancing the McCauley Helium Field, to initiate production, in Q4 2022. The Company signed the final contracts with GENRON for the construction of the McCauley Helium Field finishing facility, with all-in costs of approximately US $10,500,000. The Company plans to drill 7 offset and wildcat wells, in 2022. The Company has pre-ordered strategic components, for the Rohlfing Helium Field finishing facility. Helium is used in MRIs, in the manufacturing of fiber optics, in electric vehicles, and in space exploration to purge the rocket engines, prior to take-off.

Click here to continue... |

Interview with John Lee, CEO, Flying Nickel Mining Corp. (TSX-V: FLYN; OTCQB: FLYNF): Mining and Supplying Nickel in High-Tech Batteries, Powering Modern Electric Vehicles

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with, John Lee, who is CEO of Flying Nickel Mining Corp. (TSX-V: FLYN; OTCQB: FLYNF), a premier nickel sulphide mining and exploration Company, advancing its 100% owned Minago Nickel project, in the Thompson nickel belt, in Manitoba, Canada. The combined open pit and underground mineral resource estimate, published in 2021, includes a Measured and Indicated mineral resource of 44.23 million tonnes, grading 0.74 % nickel, for 722 million pounds of contained nickel and an Inferred mineral resource of 19.55 million tonnes, grading 0.74% nickel, for 319 million pounds of contained nickel. On August 23, Flying Nickel Mining announced that they have entered into a non-binding letter of agreement, to acquire Nevada Vanadium Mining Corp.

Click here to continue... |

Rudi Fronk, Chairman and CEO, Seabridge Gold (TSX: SEA, NYSE: SA) Discusses their KSM Project’s Outstanding Update PFS, the World’s Largest Undeveloped Gold/Copper Project

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Rudi Fronk, Chairman and CEO of Seabridge Gold (TSX: SEA, NYSE: SA), a mineral exploration company, with one of the world's largest resource bases of gold, copper and silver. Seabridge's objective is to grow resource and reserve ownership per share. Seabridge holds a 100% interest in several North American gold projects. Seabridge's assets include the KSM and Iskut projects, located in Northwest British Columbia, Canada's "Golden Triangle", the Courageous Lake project, located in Canada's Northwest Territories, the Snowstorm project, in the Getchell Gold Belt of Northern Nevada and the 3 Aces project, located in the Yukon Territory. The recent highlights, on the Company's flagship KSM project, include the NI-43-101 Technical Report, the 2022 PFS that lifts KSM profitability and sustainability to much higher levels, and the 2022 PEA that shows potential to expand mine life, for an additional 39 years, focusing on copper.

Click here to continue... |

Cobalt Blue Holdings, Ltd (ASX: COB): Ethical and Reliable Cobalt for a More Sustainable World, Transforming Global Battery Production; Joel Crane, IR/Commercial Development Manager, Interviewed

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Joel Crane, Investor Relations Manager for Cobalt Blue Holdings, Limited (ASX: COB), an exploration and development company, focused on green energy technology solutions and the development of the Broken Hill Cobalt Project, in the far west of New South Wales. Cobalt is a strategic metal, and it is in strong demand for new generation batteries, particularly lithium-ion batteries, now being widely used in clean energy systems. The main targets, for exploration, are well known, and document large-tonnage, cobalt-bearing, pyrite deposits. The project area is under-explored, with the vast majority of historical exploration, directed at or around the outcropping pyritic cobalt deposits, at Pyrite Hill and Big Hill. Cobalt Blue Holdings has designed, built, and is now commissioning and operating a Demonstration Plant in Broken Hill. The plant is aiming to treat a minimum of 3,000 tons of ore (up to 4,000 t) and produce circa 10 tons of cobalt products, (mixed hydroxide and/or cobalt sulphate).

Click here to continue... |

Stephen Hanson, Founder, President and CEO, ACME Lithium Inc. (CSE: ACME, OTCQX: ACLHF) Discusses their World Class Portfolio of Lithium Projects in the United States and Canada

by Dr. Allen Alper, PhD Economic Geology and Petrology, Columbia University, NYC, USA

We spoke with Stephen Hanson, who is Founder, President, and CEO of ACME Lithium Inc. (CSE: ACME, OTCQX: ACLHF), a lithium exploration company, with a world class portfolio of projects, located in the United States and Canada. ACME has acquired, or is under option to acquire, a 100-per-cent interest in projects, located in Clayton Valley and Fish Lake Valley, Esmeralda County, Nevada, and at Cat-Euclid and Shatford Lakes, in southeastern Manitoba. On August 17, ACME announced a significant new lithium discovery, at their Clayton Valley lithium brine project, in Esmeralda County, Nevada. This new discovery has initiated planning of Phase 2, of the drilling program. ACME Lithium is well positioned, in the growing battery and electric vehicle (EV) sectors.

Click here to continue... |

|

Click here for all featured articles...

|

|

|

Experts Corner

Stock Market Rally Could Morph Into Commodity Rally Before Downturn

by Jordan Roy-Byrne, CMT

The goldilocks market could morph into a bout of inflation before a downturn and liquidation says Gary Tanashian, editor and publisher of https://nftrh.com/.

Click here to continue... |

Interview: Key Market Signals to Watch

by Jordan Roy-Byrne, CMT

Jordan Roy-Byrne, Founder and Editor of The Daily Gold, joins us to outline why the steeping of the bond yield curve is one of the key market signals to watch for how it relates to the economic cycle, the US general equities, and precious metals markets. He outlines how...

Click here to continue... |

Video: 3 Reasons Why Juniors Have Tanked

by Jordan Roy-Byrne, CMT

Volume in junior Miners and junior exploration companies is now at a 20-year low. Share prices have plunged. Here are the causes. Click Here to Learn About TheDailyGold Premium

Click here to continue... |

Video: 3 Reasons Why Gold is Holding Up Well

by Jordan Roy-Byrne, CMT

It does not feel like Gold has held up well due to the poor performance of Silver, miners and juniors. But after the second sharpest Fed tightening cycle of the last 45 years and sharp increase in real interest rates, Gold is only 7% from its all time high. In the video we...

Click here to continue... |

Video: Stock Market Crash Declines Around Recessions

by Jordan Roy-Byrne, CMT

We show the charts and data of the stock market declines during each of the past 12 recessions. On average, the stock market makes a peak a few months before the recession and declines sharply until the recession is three to four months from its end. Thus, the length of the...

Click here to continue... |

Video: Bearish Action in Gold & Silver but Miners to Rally Next Week

by Jordan Roy-Byrne, CMT

It was an ugly week in Gold and Silver as Gold lost $1950 support and Silver plunged from $24 down to its 200-day moving average at $22. There is technical damage in the daily and weekly charts. Gold has support at $1900 but stronger support at $1850-$1865. Nevertheless,...

Click here to continue... |

Gold Market Will Turn When This Happens

by Jordan Roy-Byrne, CMT

I have written about the importance of a bear market, recession, and Fed shift for a Gold bull market. But today, I want to be more precise. There has to be a potential tipping point that precedes these catalysts. Markets anticipate the near future and...

Click here to continue... |

Video: Secular Trend in Gold & Stock Market Not Changed Yet

by Jordan Roy-Byrne, CMT

Historically, the 40-month moving average has been an excellent indicator of the secular trend in the stock market. Until the S&P 500 loses that support, it remains in a secular bull market, which means Gold and more so precious metals remain in a secular bear market....

Click here to continue... |

Video: The Turning Point for Gold

by Jordan Roy-Byrne, CMT

Significant moves in Gold and outperformance for Gold against the stock market occur when the yield curve steepens. A steepening curve precedes Fed rate cuts and usually signals a recession. Click Here to Learn About TheDailyGold Premium

Click here to continue... |

Video: Room for Small Rally in Miners but Need Macro for More

by Jordan Roy-Byrne, CMT

In this video we discuss the key support and resistance levels for Gold & Silver and opine on the potential short-term upside in the gold and silver stocks. The macro needs to align for a sustained move higher in precious metals. It’s not aligned yet. Click Here...

Click here to continue... |

The 3 Best Historical Comparisons for Gold

by Jordan Roy-Byrne, CMT

Our last article compared Gold today with the stock market in the early 1980s. Today we draw some comparisons between the Gold market at present and the Gold market at various points in the past. Gold’s status today fits elements of three past...

Click here to continue... |

How a Master Picks Gold & Silver Companies

by Jordan Roy-Byrne, CMT

Rick Rule, legendary resource investor & speculator discusses his specific process and criteria for evaluating gold and silver companies and all resource companies. Among other things, Rick details important criteria he looks for (two of the most important are people...

Click here to continue... |

Video: Gold’s 3 Best Historical Comparisons

by Jordan Roy-Byrne, CMT

There are three clear historical comparisons for Gold. These are the 1964-1965 period, the 1968-1972 period and 2009. The first is, the mid 1960s, which we argued, in another video, was the best comparison. Gold is on the cusp of a significant historical breakout. The gold...

Click here to continue... |

Video: Gold & Silver Face Weekly Resistance at $1980 & $24.50

by Jordan Roy-Byrne, CMT

Gold and Silver closed last week a tiny bit below respective weekly resistance levels at $1980 and $24.50. The bearish take is miners badly underperformed Gold the last two days, which suggests Gold weakness is coming. However, on the contrary, Silver closed the week much...

Click here to continue... |

Video: Silver Price Levels For Next 12 Months

by Jordan Roy-Byrne, CMT

In this video we evaluate the key support and resistance levels for Silver and comment on its net speculative position and open interest. The key resistance levels are $26 and $27-$28 with $22 and $20.50 being the key support levels. In the bigger picture we can simplify...

Click here to continue... |

|

|

|

|

|

|